Organisational Overview

About the Bank

Higher-tier Domestic Systemically Important Bank

Commercial Bank of Ceylon PLC is the only private sector bank in Sri Lanka designated by the CBSL as a higher-tier Domestic Systemically Important Bank (D-SIB). Total assets of the Commercial Bank Group (which comprise of the Bank and its seven subsidiaries and the associate) stood at Rs. 2.500 Tn. as at December 31, 2022 (Rs. 1.983 Tn. as at end 2021). Accounting for approximately 10.72% (2021 – 10.42%), 12.82% (2021 – 11.58%) and 12.56% (2021 – 11.82%) of sector loans and advances, deposits and assets, respectively, the Bank is the third largest bank overall in Sri Lanka, in terms of total assets, customer deposits and net loans & advances which stood at Rs. 2.426 Tn. (USD 6.610 Bn.), Rs. 1.914 Tn. (USD 5.216 Bn.) and Rs. 1.130 Tn. (USD 3.080 Bn.), respectively, as at the end of 2022 (Rs. 1.949 Tn. (USD 5.311 Bn.), Rs. 1.443 Tn. (USD 3.932 Bn.) and Rs. 1.015 Tn. (USD 2.765 Bn.), respectively, as at the end of 2021).

Hundred and Three Year Legacy

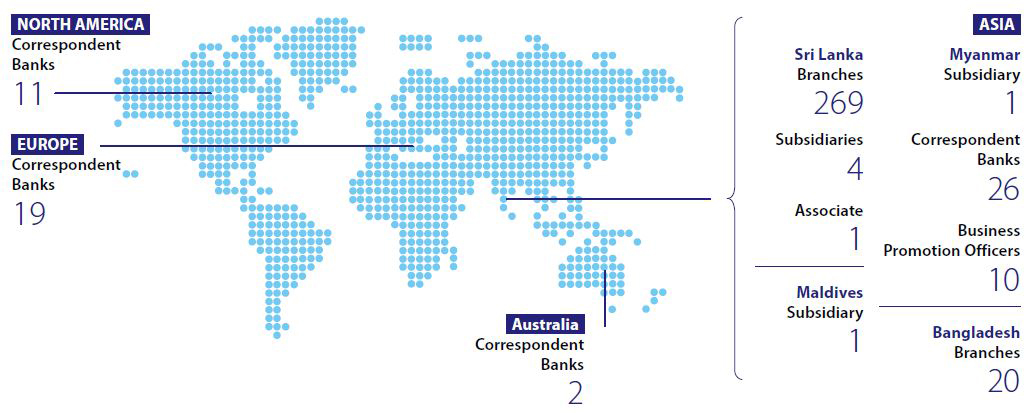

The origins of the Bank stem back to 1920 when a financial institution began its operations in Chatham Street, Colombo, embarking on a journey that saw a bank with humble beginnings reaching the pinnacle of private sector banking operations in Sri Lanka. The Bank, initially known as the Eastern Bank, marks over a half-century of operations under its present name in 2022. The journey has been one of innovating in strategic directions, evolving the banking experience of stakeholders, to create personalised banking products, including digital-first platforms that are powered by a few clicks at best. With a total staff strength of 5,121 as at end 2022 (2021 – 5,072), the Bank serves over 3.5 million customers through a wide local and international network of branches, subsidiaries, agency arrangements, Business Promotion Officers, and correspondent banking relationships.

Growing International Footprint

Commercial Bank is no longer an endemic bank but one that has consolidated an international regional presence, having built stable and innovative business operations in a gamut of locations. It began its expansion beyond Sri Lanka’s shores with the acquisition of the Bangladesh operations of Crédit Agricole Indosuez in 2003, a pioneering presence as the first private sector bank to establish a branch operation outside the country. As of today, the overseas operations have expanded into the establishment of subsidiaries in the Maldives and Myanmar. The Bank anticipates that the strategic expansion of the banking ecosystem will include a wider geographical presence in the regional landscape of South Asia in the future, in line with its Vision given in the Inner Front Cover.

Risk Profile

In April 2022, reflecting heightened near-term downside risk stemming from constrained access to foreign-currency funding and the resulting indications of stress experienced by the banks in the system, exacerbated by the sovereign‘s credit profile, Fitch Ratings Lanka Ltd. (Fitch) changed Commercial Bank’s National Long-term Rating from “AA-(lka)/stable outlook” to “AA-(lka)/Rating Watch Negative” along with 12 other banks. In January 2023, following the sovereign downgrade and recalibration of Fitch’s Sri Lanka National Rating Scale, Fitch downgraded the Bank’s National Long-term Rating from “AA-(lka)/Rating Watch Negative” to “A(lka)/Rating Watch Negative” along with nine other banks. Meanwhile, the Bank’s Bangladesh Operations’ credit rating was reaffirmed at AAA by Credit Rating Information Services Ltd. in June 2022 for the 12th consecutive year. The ratings reflect the Bank’s intrinsic financial strength, the established domestic franchise as Sri Lanka’s third-largest bank and the entrenched domestic deposit franchise that underpins the Bank’s funding and liquidity profile.

Diversification

The Bank’s business is well-diversified across four main business segments – Personal Banking, Corporate Banking, Treasury, and International Operations. The International Operations of the Bank, which accounted for 16.92% of consolidated assets as at December 31, 2022 (2021 – 12.83%) and 71.10% of consolidated profit before taxes for the year ended December 31, 2022 (2021 – 19.45%), covers operations in Bangladesh, the Maldives, Italy (under voluntary liquidation), and Myanmar. Besides geographical diversification, the Bank has successfully achieved a high level of diversification in its operations across many other parameters such as customer profile, currency, products and services portfolio, interest rate type, funding profile, maturity profile, economic sectors and the sources of revenue given on Sustainable banking – Value creation.

Vibrant financial intermediation

Commercial Bank became the first private sector bank in Sri Lanka to have three key balance sheet indicators to surpass Rs. 1 Tn., having crossed Rs. 1 Tn. mark in assets, deposits and the loan book in 2016, 2019 and 2021, respectively. As a leader in financial intermediation, 78.92% of the total assets of the Bank are funded by customer deposits (2021 – 74.03%). The Bank’s loans to deposits ratio has been over 70% on average for the past five years consecutively, reflecting a growth in loans commensurate with the growth in deposits. The Bank’s asset quality is one of the best in the industry, while its Current Accounts and Savings Accounts (CASA) is the highest among the peer banks accounting for 38.36% of total deposits as at December 31, 2022 (47.83% of total deposits as at December 31, 2021).

Capital position of the Bank

The Bank’s Tier 1 Capital Ratio and Total Capital Ratio stood at 11.389% and 14.657%, respectively, as at December 31, 2022 (11.923% and 15.650%, respectively, as at December 31, 2021), compared to the regulatory minimum ratios of 10% and 14% applicable for the year. The Bank’s growth has been prudent with gearing in terms of on-balance sheet assets as well as risk-weighted assets remaining at 11.91 times and 6.82 times, respectively, as of the end of 2022 (11.82 times and 6.39 times, respectively, as of the end of 2021). Demonstrating the strength of the franchise, the Bank’s shares reported a book value of 0.31 times and a market capitalisation of Rs. 61.591 Bn. (USD 167.824 Mn.) among the banking sector on the CSE at year’s end, the Bank is the 12th largest institution listed on the CSE overall.

Ownership of the Bank

Of the 17,022 ordinary voting shareholders of the Bank at end of 2022, DFCC Bank PLC held 12.12% and entities related to the State, including Employees’ Provident Fund, Employees’ Trust Fund Board and Sri Lanka Insurance Corporation, collectively held 18.95% of Bank’s shares. Mr Y S H I Silva (9.90%), Mr D P Peiris (7.71%), the International Finance Corporation (IFC) (7.11%), Melstacorp PLC (4.14%), CB NY S/A IFC Emerging Asia Fund LP (3.67%), CB NY S/A IFC Financial Institutions Growth Fund LP (3.67%), and Mr K D D Perera (3.67%), are the other major shareholders, holding a combined ownership stake of 39.87%. Notably, the Bank’s foreign shareholders have a combined stake of 17.26% in ordinary voting shares as at end of 2022.

Most awarded Bank

The heavily awarded and accoladed status of the Bank has made it the most awarded bank in the country, bearing testimony to its commitment towards good corporate governance. The Bank won 50 international awards and 11 local awards during the year under review. These included, among others, Best Bank in Sri Lanka by The Banker Magazine UK, Strongest Bank in Sri Lanka by The Asian Banker Magazine UK, Global Performance Excellence Award World Class by Asia Pacific Quality Organisation, and National Quality Award by Sri Lanka Standards Institute. Refer Sustainable banking – Value creation for the details of awards and accolades won during the year.