Management Discussion and Analysis

Sustainable Banking – Value Creation

Commercial Bank operated with due vigilance in 2022, carefully managing the many risks associated with financial intermediation and maturity transformation. Such a cautious approach was adopted by the Bank to ensure responsible value creation for its diverse stakeholders. The lending portfolio of the Bank which is continuously exposed to risk-elevated environments has readily reformulated the ongoing risk management practices, to minimise risks and to bring enhanced prudence into the Bank’s multifaceted approaches to stay relevant and timely. The domino effects of the Easter Sunday carnage of 2019, the COVID-19 pandemic, the continuing war in Ukraine, the disruption of supply chains, the turmoil in the political landscape in Sri Lanka flaring public sentiment, have collectively encumbered the Bank’s operational environment in 2022. Still, the above realities require recognition to manage the risk-elevated landscapes with prudent planning, driving reciprocals of mutual growth.

In such a risk-elevated environment, the Bank must be a stable and responsible value creator to ensure that the stakeholders are empowered by the Bank’s continuance to be the center of their financial ambitions. For the Bank, partnerships come in many forms, including those with investors, customers, employees, Government institutions and regulators, business partners, and society and environment, the key stakeholders of the Bank, forming a collective who are mutually dependent on each other for their enterprise and wellbeing. Delivering responsible financial products is the primary charter of the Bank that continues to leverage strengths while learning from everyday experiences to enhance the financial security of all its stakeholders.

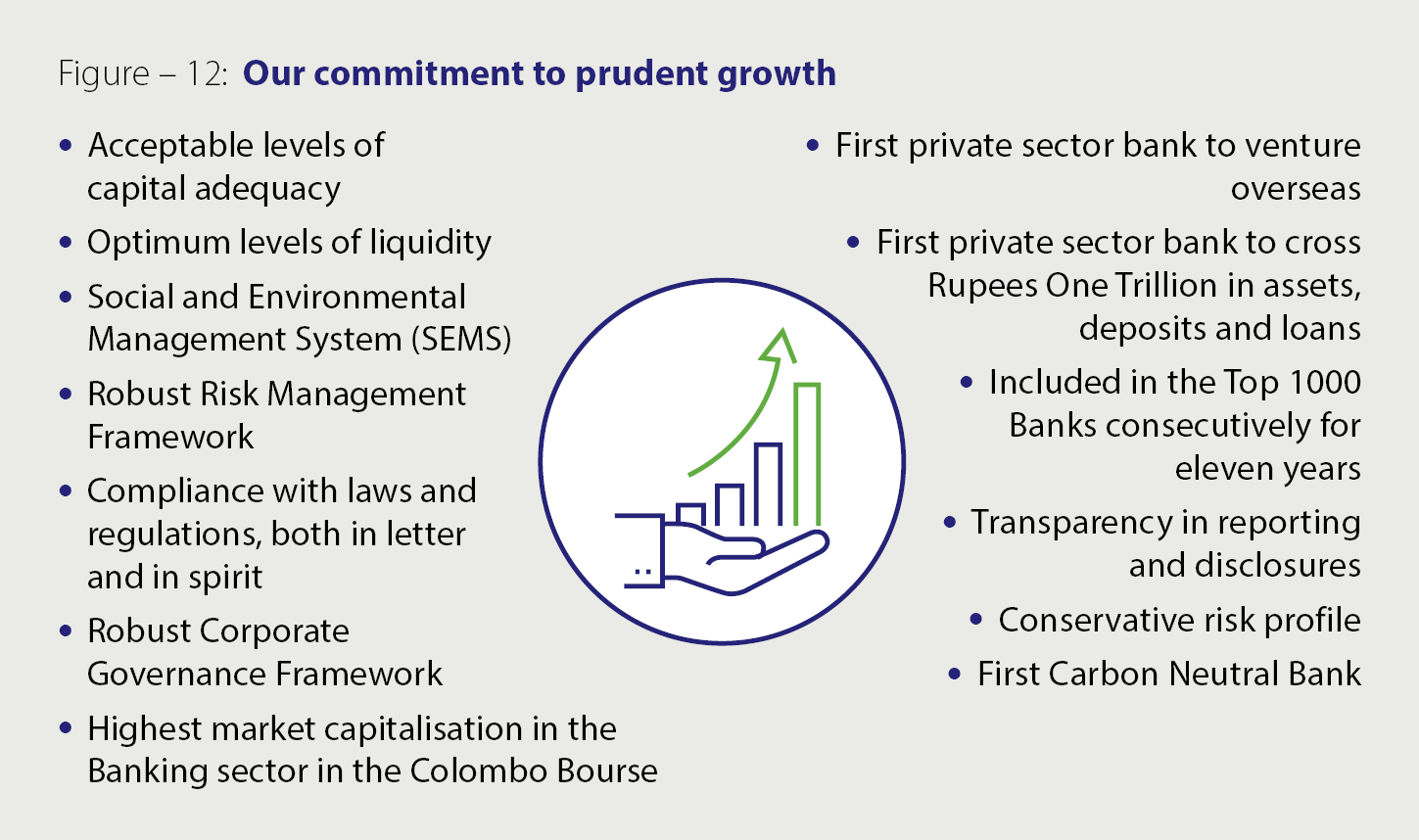

1. Prudent growth

Prudent growth, in a risk-elevated operating environment both locally and globally, is a careful convergence of leveraging strengths, profiting on selected opportunities, managing risks, and minimising the impacts of threats. In the unprecedented operating context that prevailed during 2022, the biggest challenges for the Bank were maintaining healthy liquidity, capital buffers, and foreign currency reserves. The rating downgrades of Sri Lanka made it challenging for the Bank to operate in international markets to raise the much-needed foreign currency liquidity. Furthermore, containing Non-Performing Credit Facilities (NPCF) whilst generating growth amidst rising inflation and a falling currency and loan book expansion in a milieu of increasing interest rates were key challenges the Bank had to contend with.

As the largest private sector commercial bank in Sri Lanka, that has garnered the trust of over 3.5 million customers, Commercial Bank was cognisant of its fiduciary responsibility of governing the Bank’s affairs meticulously and ensuring it is adequately capitalised. Even as Prudent Growth represents value creation for all its stakeholders through the short, medium, and long-term, the Bank continued to focus on agility of operations, innovation, the evolution of the workforce, managing risks, and exemplary governance to drive growth.

A crucial aspect of prudent growth is ensuring the stakeholders are protected from exterior and interior stresses. The below narrative accentuates how the banking ecosystem navigated prudent growth making holistic sustainability the eye of the storm, the calm in the wake of multiple disruptions that saw the Bank to serener times. Prudent growth is not just the big picture, but the forensic detail in which the Bank navigates its operations to instill protection of its key stakeholders. Such meticulous management of operations sets a precedent in how a bank should function to cultivate safety and sustainability as its core strengths in disruption-plagued times.

Creating long-term value: Striving to enrich

The Bank is positioned to take on the challenges confronting the banking sector and provide stability to the economy. Commercial Bank has built a reputation as a franchise that engages in sustainable value creation for its stakeholders. The Bank has a strong presence locally as well as a footprint regionally, enabling financial leveraging, and influencing a myriad of spheres, each consisting of a gamut of stakeholders.

The Bank’s prudent risk appetite has been a yardstick for stability, with a strong stakeholder base that entrusts the Bank with value creation using its array of financial products and services.

The Bank’s dominant export market share, success in the worker remittances business, healthy CASA ratio, and the strength of its overseas operations, specially in Bangladesh and Maldives has afforded a greater resilience to the Bank. The Bank’s reputation within the international sphere is unblemished and outstanding, just as its stellar corporate image within the country, making it easier to get things done internationally. Furthermore, the comprehensive governance and risk management frameworks ensure maximum coverage and readiness for risks and opportunities to convert them into a sustainable financial performance. The loyalty of the customers, who have been with the Bank for generations, has enabled it to be the leader in all key spheres of banking – retail, corporate, and SMEs – allowing the Bank to be more prudent and quality-conscious about its debt portfolio. The dynamic and thoroughly professional team is geared to face any challenge head-on and build lasting relationships with the Bank’s customers to offer them feasible solutions.

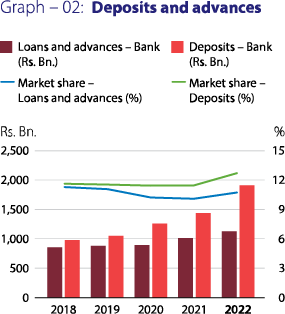

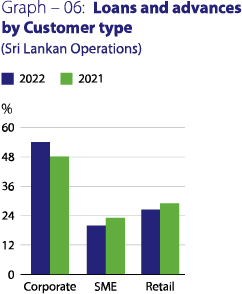

In 2022, the Bank’s deposit base grew by 32.66% to Rs. 1.914 Tn. with a CASA ratio of 38.36% while the gross loans and advances grew by 13.07% to Rs. 1.220 Tn. by the end of the year.

Table – 08: Growth in deposit base and lending portfolio over the past decade

| 2022 Rs. Tn. |

2012 Rs. Tn. |

10-year CAGR (%) |

|

| Deposit base | 1.914 | 0.391 | 17.23 |

| Gross Loans and advances | 1.220 | 0.386 | 12.20 |

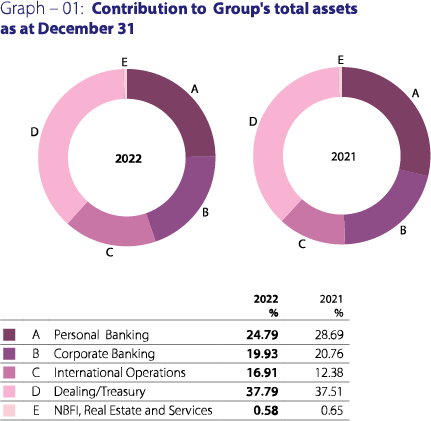

A diversified Bank: A multitude of mixes

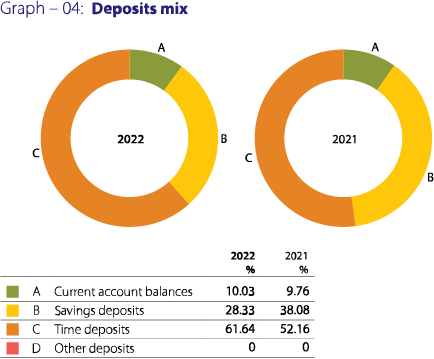

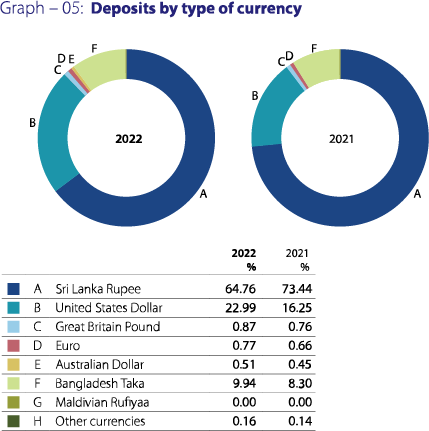

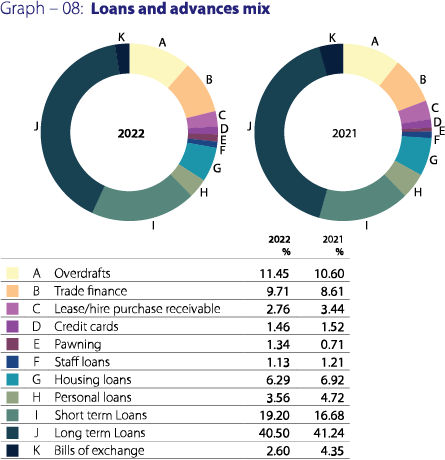

Diversification was an actuality in regional geography, customer profile, banking channels, the repertoire of products and services, and the currency mix of the Bank, among other factors. Diversification is a risk management tool to offset acute setbacks, perform better when faced with volatilities, and remain agile amidst changing market conditions. The Bank’s diversity is accentuated by the following parameters that are in place.

- Geographically: Sri Lanka, Bangladesh, The Maldives, Myanmar, and a number of Business Promotion Offices (BPOs) across the Middle East and Korea (Refer Graph 45 on page 217)

- Customer Profile (Refer customer segmentation – Table 09)

- Multiple Banking Channels (Refer channel mix – Table 10 on page 66)

- Currency-wise Product Mix [Refer Notes 33.1 (b) on page 297 and 45.1 (b) on page 326]

- Products Portfolio [Refer Notes 33.1 (a) on page 297 and 45.1 (a) on page 326]

- A Myriad of Funding channels (Refer Table 10 on page 66 and funding diversification by product on page 62)

- Maturity Profile (Refer Note 60 to the Financial Statements on pages 348 and 349)

- Economic Sectors [Refer Note 33.1 (c) to the Financial Statements on page 298]

- Sources of Revenue (Refer Notes 13.1 and 14.1 to the Financial Statements on pages 272 and 274)

Staying well capitalised: Steering through a tempest

The Bank’s sustainability hinges on a strong base of capital that acts as a cushion or a shock absorber against unexpected losses and as a regulatory restraint on unjustified asset expansion. A crucial aspect of the Bank’s success is the loyal shareholder base the Bank can rely on for more capital whenever the need for a capital infusion arises. A bank needs capital to acquire the required fixed assets to establish, perpetuate, and expand business. To ensure that banks are adequately capitalised to meet its obligations to the stakeholders, tightened regulatory requirements and more stringent reporting standards have been imposed all in the interest of various stakeholders, depositors in particular.

In 2022, there were difficulties in securing capital due to the convergency of a multitude of factors. The CBSL implemented several measures to provide banks with more flexibility and opportunities to operate in these challenging conditions and support economic recovery while taking measures to improve their safety and soundness. The measures included, among others, permission for banks to draw down on their Capital Conservation Buffers (CCB) to ensure that banks have an additional layer of usable capital that can be drawn down during times of stress, extending the timeline to restore the CCB requirement within three years based on a Board approved capital augmentation plan, and granting flexibility to stagger the unrealised mark to market loss on Government Securities denominated in LKR.

To assess its capital requirements, the Bank uses the Internal Capital Adequacy Assessment Process (ICAAP), and the annual strategic planning and budgeting exercise. Furthermore, the Bank uses Risk-Adjusted Return on Capital (RAROC), prudent capital allocation, controlled growth in risk-weighted assets, expansion of fee-based services, timely pricing/re-pricing of its assets and liabilities, prudent dividend policy, well-diversified products and services portfolio, Recovery Plan and capital instruments to manage its capital requirements. Through these measures, the Bank has been able to consistently maintain its capital adequacy ratios at the required levels.

Optimising financial resources: The epicenter

Treasury is a key function that is vital to the financial health and success of the Bank. Whilst helping the Bank to optimise financial resources and manage financial risks effectively, the strategic role of the Treasury in supporting operations has been enhanced to help the Bank to achieve prudent growth.

In a climate of limited access to international markets due to the downgrading of the country’s credit rating, declining foreign remittances, steep depreciation of the currency, and a 700 bps rise in domestic interest rates, 2Q of 2022 was the most challenging for the Bank’s Treasury. Official reserves dropped from USD 7.6 Bn. in 2019 to less than USD 400 Mn. (excluding a currency swap equivalent to USD 1.5 billion with China) in June 2022.

The Bank’s Treasury navigated the challenging context by conducting derivative transactions, exploring opportunities for overseas expansions, expanding networking sessions, and launching an online platform for foreign exchange (FOREX) transactions to augment the FOREX position of the Bank. Several client awareness sessions including client meetups were conducted to strengthen client relationships and secure new business opportunities. Furthermore, the client value proposition was enhanced by offering structured packed solutions and designating a Treasury Relationship Manager for each account. The competencies of the Treasury staff were augmented through training and development and recruiting new talent with the required expertise to deliver an exceptional client service. Going forward, the Treasury aims to implement a treasury system, engage in talent development, expand the derivatives portfolio, restructure the Fixed Income Securities (FIS) Portfolio, approach specific export segments with added incentives to increase volumes, and automate the FX portal.

Diversification

OPERATING SEGMENTS

Excluding unallocated/eliminated adjustments

SOURCES OF FUNDS

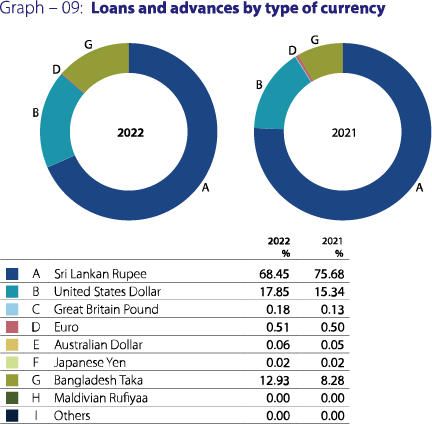

LOANS AND ADVANCES

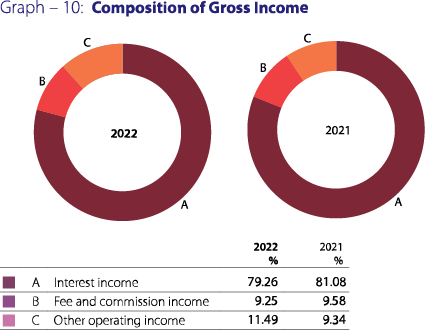

GROSS INCOME

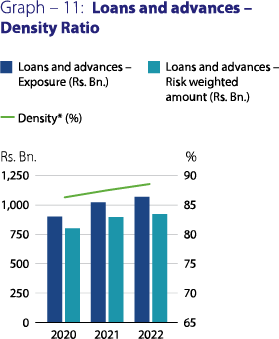

RISK PROFILE OF THE LOAN BOOK

* Density - Risk weighted assets expressed as a % of total exposure

Capital management objectives: Rules and local practices

The Bank accords highest importance to capital management whereby measures are taken to ensure availability of sufficient capital at all times through its ICAAP, with the following objectives:

- Adhering to industry standards and an even more stringent internal capital adequacy requirement, the Bank remains well capitalised, above the minimum regulatory requirements

- Ensuring maximum profitability through optimum capital usage

- Being supportive of wealth creation and business expansion

- Supporting a credit rating that is well above industry peers

For more information on Bank’s Capital Management, please refer page 203 on Risk Governance and Management section, Note 66.5 on pages 385 and 386 and page 416 for Annex 2, Disclosure 7 on Summary discussion on adequacy/meeting current and future capital requirements.

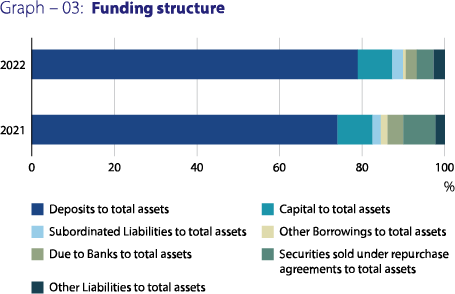

Managing funding and liquidity: Honouring commitments

A liquidity foundation that can sustain the Bank in relation to ad hoc, acute, and unforeseen shocks, is now part of the banking resources, abiding by Basel III regulations, that introduced Liquidity Coverage Ratio (LCR, 2015) and Net Stable Funding Ratio (NSFR, 2019) as prescriptive thresholds. The Bank’s reputation as an outfit that does not compromise its liquidity status has ensured that the stakeholders have confidence in the banking stalwart. The Bank’s ALCO meets at least on a fortnightly basis to ensure that funding and liquidity are consistent with the Bank’s overarching assurances to its stakeholders. ALCO actively deliberates on market liquidity, foreign currency funding position, current and perceived interest rates, changes in policy rates, credit growth and alternative investment options for its excess funds given the low growth in loans and advances.

The Bank has faced challenges in its funding and liquidity management. The acute decline in foreign currency reserves and the relegation of the sovereign status, which together played a role in presenting a challenging environment to secure foreign exchange was a key challenge. In such a climate, the Bank proactively responded by adopting new funding strategies while also reaching out to new funding partners.

The Bank’s funding sources for onward lending, in order of their assessed stability include:

- Retail deposits mobilised through the branch network

- Low-cost foreign currency borrowing (provided the interest and swap cost attached to such borrowing is cheaper as compared to the cost of wholesale deposits)

- Selected long-term wholesale deposits

- Re-purchase agreements

- Subordinated debentures

The Bank’s investment banking arm continued to embrace sustainability by balancing traditional investing with ESG insights to improve long-term outcomes. The year 2022 was a relatively inactive period for the investment banking arm of the Bank. The Rs. 10 Bn. debenture issue managed by the Investment Banking Unit further strengthened the Tier II capital base of the Bank, bridged maturity mismatches in the assets and liabilities portfolio of the Bank, and raised funds for the expansion of the Bank’s lending portfolio, especially in the SME segment and export-oriented industries in the interest of supporting the national economy. The debenture which closed within hours of opening after it was oversubscribed on the opening day reflects the investor confidence in the Bank, amid the challenging operating environment.

Funding and liquidity management objectives: Managing worth

The overall objectives of the Bank’s funding and liquidity profile encompass the following efforts on the part of the Bank:

- Honouring the stakeholders’ varied transactions with the Bank, inclusive of deposit maturity withdrawals and a multitude of cash commitments in the normal environment as well as in times of financial constraints and economic hardships.

- Remaining compliant with all regulatory and reporting standards, building the internal funding and liquidity targets to reach beyond the benchmarked thresholds, thereby having internal standards in place that are more stringent than broader prescriptive measures.

- Maximising profitability through the optimal deployment of liquid assets, both as short-term measures as well as leveraging intelligent and judicious planning for the longer term.

- Funding future business expansion at optimum cost.

- Supporting the desired credit rating.

- Complying with Basel III regulatory measures in funding and liquidity requirements (Refer Annex 2, Basel III – Disclosures under Pillar III).

Anti-Money Laundering (AML): Brilliant and white

The Bank performs Money Laundering and Terrorist Financing risk assessments to ensure that its reputation is not tarnished by such illegal activities. Guided by the relevant regulatory directions and internal policies, such risk assessments are conducted by the Bank at the time of onboarding customers as well as at set periodic intervals based on their perceived risk levels thereafter with the help of the algorithms built into the computer systems. The AML/Compliance Department periodically reports its findings and observations to the Board through the BIRMC in addition to the monthly statutory reporting to the Financial Intelligence Unit of the CBSL.

Anti-bribery and anti-corruption: Perfect altitudes

The Anti-Bribery and Anti-Corruption Policy of the Bank leverages to uproot all sorts of misdeeds that are criminal in activity. In affirming its commitment to the 10 principles of UNGC, while ensuring that the merits of the Code of Ethics are vigilant and practiced, the Bank expects all its employees to abide by the highest standard of ethical conduct, with a zero-tolerance policy for any abuse of power, solicitation, or acceptance of bribes, even trickles of corruption, as well other contentious and unlawful behaviours that taint the banking culture. The Bank also ensures that all subcontractors, vendors, suppliers, service providers, consultants and representatives, and others who are providing a service to the Bank, abide by the highest level of ethical conduct that is part and parcel of the banking outfit. Furthermore, the Bank is guided by the Whistleblowers Charter and guidelines that covers aspects such as accepting and offering gifts or other illegal gratification, collection and borrowing of funds, obtaining undue favours from customers and suppliers, and holding a Directorship, being a Partner or Shareholder in private companies enumerated in the Code of Ethics and Administrative Circulars. The Board approved Anti-Bribery and Anti-Corruption Policy is available on the Bank’s website.

Ethics and conduct: Uncompromised virtue

The Bank conducts itself with a maximum commitment towards ethics and conduct standards that are both written into prescriptive compliance standards and the de facto measures that are goodwill-based and ethically proactive, to stay true to being a virtuous agent of the highest ethical standards. Taking a zero-tolerance attitude towards bribery, corruption, fraud, money laundering, and other corporate vices, which is a benchmark of the Bank’s line of conduct that is periodically audited (the scope and frequency of audits are put in place by the Inspection Department) to safeguard best practices that are intolerant of any presence of misdeeds. The code of ethics that the Bank abides by is reinforced by an active whistleblower policy that promotes a culture of reporting any unethical practices such as corruption, fraud, and misappropriations to the Compliance Officer in order, to ensure that the Bank’s integrity is untainted of such misdoings.

Conduct Risk Management Policy Framework: Staying one step ahead

During the year, the Bank adopted a Group Conduct Risk Management Policy Framework with a view to further strengthen risk management and corporate governance by ensuring that the Bank does not engage in any action that harms customers, negatively impact market stability and prevent effective competition. It is expected to establish a risk culture that not only addresses the risk of misconduct but also highlights clear accountability of actions through a preventive approach, by ensuring proper customer onboarding practices and transparency in fees and charges while avoiding fraudulent activities, insider trading, improper financial advice to customers, mis-selling of financial products, tax avoidance, collusion with financial markets and inaccurate financial and regulatory disclosures.

Socially and environmentally sustainable lending and practices: A green ethos

More detailed coverage of green finance measures implemented by the Bank in the year 2022, inclusive of the internal taxonomy as well as the regulatory-compliant prescriptive reporting standards (external taxonomy) that were put in place by the CBSL, are described under Green and Safe Workplace under “Responsible Organisation”.

The Green Finance vision of the Bank is to support green initiatives and the green portfolio to a significant part of the Bank's lending portfolio. The Bank has been the recipient of two awards for its performance in climate financing and environmental consciousness for the year 2021 from IFC. IFC has reaffirmed Commercial Bank of Ceylon’s status as the South Asian financial institution to record the highest number of climate finance transactions in fiscal year 2022, awarding Sri Lanka’s benchmark private sector bank the prestigious Climate Assessment for Financial Institutions (CAFI) award in respect of the year. The CAFI Award for climate reporting was conferred on Commercial Bank for successfully completing 314 climate finance transactions that met IFC’s climate eligibility criteria. The CAFI tool was used to assess climate eligibility and measure the climate impact of investments.

The Bank uses its SEMS to keep a foothold on the social and environmental risks that could be set in motion by the funding activities while helping the borrowers to upkeep and maintain the obligatory requirements in green financing.

The Bank’s green financing portfolio has made strong inroads in ensuring that its carbon footprint is reduced by 229,752.47 tCO2e upto December 31, 2022.

2. Customer centricity

Based on a deep understanding of its customers in terms of their expectations, needs, preferences as well as concerns and responding with products and services that are required through their journey, the Bank makes every attempt to offer an unparalleled banking experience, making every interaction with the Bank a pleasant experience. In the rapidly changing operating context, it requires transforming internal mindsets and processes to remain agile and relevant. The Bank has carefully segmented its diverse customer base and tailored its services to cater to each segment, enabling the Bank to deliver a differentiated value proposition that enhances its brand and elevates customer loyalty. Meeting the needs of customers, and providing such personalised support was vital in a year of unprecedented economic downturn.

Customer segmentation: Tailor-made solutions

The Bank continued to deliver an unparalleled banking experience to its customers and responding with products and services that meet and even exceed their expectations. This involved transforming internal mindsets and processes to remain agile and relevant.

To cater to its diverse customer base with tailor made solutions and offer a differentiated value proposition, the Bank segments each of its customer base. This helps to elevate the Commercial Bank brand and strengthen customer loyalty and engagement as depicted on tables 09 and 10 below.

In order to measure satisfaction among customers, the Bank engaged the services of Kantar Research. The Bank achieved a total TRI*M score of 101 for Corporate Banking which is well above the average to the regional benchmark of 85. Values between 100 – 150 is the highest tier denoting excellence. The TRI*M score for Retail Banking was 85, the highest among the competitors who on average scored 74. The Bank secured the second highest TRI*M score of 92 for SME Banking.

Table – 09: Customer segmentation

| Criteria | High net-worth | Corporate | SME (Small and Medium Enterprises) |

Micro customers | Mass market |

| Income/Size of relationship/Business turnover/Exposure | Individuals with banking relationships above set thresholds | Annual business turnover> Rs. 1.0 Bn. or Exposure> Rs. 250 Mn. | Annual business turnover< Rs.1.0 Bn. or Exposure< Rs. 250 Mn. |

Exposure< Rs. 500,000 |

Individuals not falling into other categories |

| Price sensitivity | High | High | Moderate | Low | Low |

| Products of interest | Investment | Transactional, trade finance, and project loans | Factoring, leasing and project financing | Transactional | Transactional |

| Number of transactions | Low | High | High/Moderate | Low | Low |

| Level of engagement | High | High | High | Low | Low |

| Objective | Wealth maximisation | Funding and growth | Funding, growth and advice | Funding and advice | Personal financial needs |

| Background | Elite business community/ professionals | Rated, large to medium corporates/MNCs |

Medium business | Self-employed | Salaried employees |

| Number of banking relationships | Many | Many | A few | A few | A few |

| Level of competition from banks |

High | High | Moderate | Low | Moderate |

Table – 10: Channel mix and target market on perceived customer preference

| Customer segment | Branches | Internet & Mobile Banking |

ATMs/CDMs CRMs |

Call centre | Relationship managers |

Business promotion officers |

Premier banking units |

| High net-worth | |||||||

| Corporates | |||||||

| SMEs | |||||||

| Micro | |||||||

| Millennials | |||||||

| Mass market |

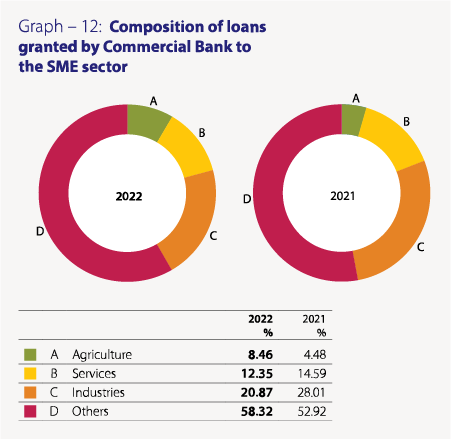

Uplifting the Small and Medium Enterprises (SMEs): Lending matters

Commercial Bank was declared the largest SME lender for 2020 and 2021, by the Ministry of Finance, Sri Lanka, which speaks amply of the Bank’s focus and commitment to the SME Sector.

Capacity building of SMEs that form the backbone of the Sri Lankan economy is an ongoing and overarching demand for the Bank that has a resolute pipeline of financial products and services. In such a climate, developing the financial literacy and capacity building of the SMEs takes precedence. The Bank conducted webinars on how to penetrate diverse markets, leverage non-financial services, and connected SMEs with both supply chains and exporters. The Bank also enhanced the literacy of SMEs in areas such as entering the export market, marketing a product, and utilising the toolboxes of international methodology to enter untapped or under-tapped markets. During the year under review, the Bank conducted awareness programs on diverse subjects for over 800 micro-SMEs (MSMEs), Women SMEs (WSMEs), and future SMEs. Details of the SME training programmes conducted are given on page 68 of this Report.

Furthermore, the Bank conducted SME fairs and SME clinics, the former to introduce a centralised event to develop networks, and the latter on how best to resolve the impending problems and to transpose the SME business to a whole new echelon. In particular, the Bank concluded its first of a kind, two-day “SME Trade Fair” at Diyatha Uyana, Battaramulla with the participation of over 110 SMEs. A one-stop information center with the participation of various Government and other stakeholder institutions was set up at the event to provide services to the SME sector. The Bank continued to promote digital banking products among SMEs that participated at the Trade Fair to minimise operational costs and improve efficiency.

The ComBank BIZ Club launched in 2017 continued to provide SMEs with extensive networking opportunities and other benefits beyond lending. The number of members has grown to over 5,000, comprising 50% of the Bank’s SME portfolio as of December 31, 2022. The Bank continued to offer several benefits to the members of the Club including free financial advisory services and invitations to exclusive business seminars, which are beneficial to the development of their businesses. To date, the Bank has assisted over 12,000 MSME customers through 1,215 financial literacy programmes.

The Bank took an initiative to broad base microcredit facilities to better sustain the MSMEs in an impending crisis. The small business custodians were armed with microfinancing to help MSMEs to face the incumbent situation, to tap into the value creation processes of the Bank, in order to better navigate the testing times. A Business Rehabilitation & Revival Unit was set up to assist SMEs to revive and recover from the dragged-out financial crisis, and to help them come out of their stagnancy. The Bank also took initiatives in NPCF management, redeployment of staff, implementation of regional rehabilitation centers, and loan delinquency management, to help SMEs.

In the backdrop of the tough economic conditions, the Bank closely collaborated with the SMEs to offer concessions by restructuring and rescheduling loan facilities. The SME officers were trained to better understand the SMEs and to instill in them adaptable practices to facilitate the recovery of the SMEs of concern. The moratoriums offered to SMEs are maturing in January 2023 and in such a landscape, the required repayment schemes, and the restructured loans with concessions were put in place to ensure a lifeline for the hardest-hit SMEs in 2023 and beyond. As per the CBSL instructions, the Bank considered special moratoriums for loans for the value of Rs. 174.921 Bn. of which Rs. 41.429 Bn. represented SMEs.

For proactively identifying the timely needs of SMEs and micro enterprises and providing tailor-made products and services to assist this segment that has in the past two years been affected first by the pandemic and subsequently by economic shocks and funding issues, the Bank was recognised as the “Best Bank for SME Banking” in 2022 by the respected Asiamoney Magazine.

Source: Annual Report 2021 Ministry of Finance Sri Lanka

Financial altruism: The gift of giving

The Bank continued to be a driving force in partnering and cooperating with national economic development efforts, playing a significant role in the post-pandemic recovery process. Stretching beyond the mandated debt moratorium measures, the Bank granted working capital loans and concessions to affected sectors, whilst building on its post-COVID momentum in rolling out relief programmes, having emerged as the leading lender and provider of relief amongst private sector banks during COVID-19.

Segment analysis of customers who availed concessions/moratoriums under the CBSL Directions

| As at December 31, 2022 | ||

| Segment | No. of loans | Balance outstanding (Rs. Bn.) |

| Corporate | 767 | 89.549 |

| Retail | 26,850 | 43.105 |

| Agriculture | 263 | 0.783 |

| Micro | 796 | 0.056 |

| SME | 6,238 | 41.429 |

| 34,914 | 174.921 | |

Note : The figures include both the active and expired moratoriums.

Supporting exporters: The quintessential exports Bank

Commercial Bank which channels 18% of Sri Lanka’s export volumes, entered into a strategic partnership with the National Chamber of Exporters of Sri Lanka (NCE) to create another platform to extend financial solutions to Sri Lanka’s exporters, with due emphasis on SMEs. This is an extension of the Bank’s commitment to encourage and strengthen SMEs engaged in the export market, and the delivery of a full range of international banking capabilities and expertise to facilitate the growth of business for exporters. Exporters had also the opportunity to take part in a Trade Fair, Seminars and Webinars organised by the Bank in collaboration with industry experts such as the EDB and the Ministry of Commerce during 2022.

Female participation: A kaleidoscope

A series of women-centered programmes and events took place at several branches of the Bank in March 2022 to commemorate International Women’s Day, while dedicating the first quarter of 2022 to its flagship Anagi Women’s Banking portfolio.

On top of the “Anagi Women’s Savings Account” a new loan scheme that allocates an expanded portfolio of initiatives designed exclusively to support the aspirations of women was launched during the quarter. The new loan product portfolio – “Anagi Business Loan for Women Small and Medium Entrepreneurs (WSME)” was designed in collaboration with the IFC – under the IFC – DFAT Women in Work programme agenda, a Gender Advisory Project – using its expertise in increasing access to finance for women, an important but under-served segment.

Women from many professions and careers were felicitated in 2022, including female doctors, assistant government agents, accountants, nurses, principals, senior teachers, media personalities, lawyers, women’s society leaders, beauticians, police officers, artists, micro, small and medium entrepreneurs, and women in the agriculture, health and garments sectors.

The Bank also deployed its Bank on Wheels service to many areas of the country, especially garment factories, to facilitate the opening of Anagi Savings Accounts that are designed to support the dreams and aspirations of women. The Anagi Instant Personal Loans were launched to empower employed women receiving their salary via PayMaster.

During the year 2022, the Bank also conducted capacity-building programmes for 425 women entrepreneurs.

The Bank partnered with the PIM to sponsor certificate courses for 50 female entrepreneurs on Women Entrepreneurship Skill Development in Colombo covering two Colombo regions, and successfully conducted the 2nd session in Kandy covering Central, North Central and Wayamba regions. Additionally, the Bank conducted a Career Guidance program for 75 female students at the University of Colombo. Through all non-financial programs, the Bank was able to support more than 1,000 students, WSME customers, and non-customers in 2022.

Considering the entire SME loan portfolio of the Bank as of end of 2022, women-connected SMEs stand at 50% (48% in 2021). The Bank has over 14,000 women connected SME facilities and over 5,600 SME women connected customers. Furthermore, from the entire retail loan portfolio of the Bank, women-connected retail loans at the end of years 2021 and 2022 stood at 30.65% and 32.02% respectively. Compared to 2021, in the year 2022, the women-connected retail loan portfolio growth is 1.37% equalling to Rs. 2.5 Bn.

With the relaunch of the Anagi brand in the year 2022, the Bank was able to open over 92,000 new Anagi Women’s Savings accounts with a growth of 39.4% compared to the previous year. Further, the total deposits held by female customers increased from Rs. 545 Bn. to Rs. 697.5 Bn. in 2022 compared to 2021. New female customer base growth recorded a 16.5% increase in 2022 compared to 2021.

Empowering futures: A cosmopolitan tomorrow

The Bank embarked on a new chapter in consolidating the futures of children in an ever-expanding global village by launching the Arunalu Foreign Currency Minor’s Savings Account. The savings account can be opened in four designated currency denominations for children who are Sri Lankan citizens residing in Sri Lanka or for children of Sri Lankan emigrants whose birth is registered in Sri Lanka. Through this account, the Bank provides the opportunity to parents to start saving early against the future expenses of their children, especially for higher education in a foreign country, without the risk of being affected by the impacts of the depreciation of the Rupee. The account can be opened with a minimum initial deposit of USD 50 or the equivalent in other designated currencies. The total savings of an account can be cashed on the 18th birthday or later by the account holder.

Senior citizens’ accounts: Troves not just of wisdom

The Bank widened its senior citizen account holder base by relaunching its “Udara” Senior Citizens Account with new features and special interest rates and offering more rewards. The minimum initial deposit was reduced from Rs. 5,000 to Rs. 1,000 and Udara Fixed Deposits were offered from Rs. 10,000 upwards. Among the new features are the introduction of a Statement Savings Account in addition to the existing Passbook Savings Account, and offering ePassbook and eStatement facilities free of charge. Furthermore, Udara customers are accorded priority service at any Commercial Bank branch upon submission of their passbook, debit card, or special identity card.

Agriculture: Sustainable finance that feeds

The Bank launched the Dirishakthi Value Chain Development Programme to support microentrepreneurs with a holistic intervention. This encompasses financing and empowerment activities that benefit the borrowers and all participants in their value chains to drive success and growth from the grassroots level. Its In-kind Grants initiative was introduced to support the identified value chains to improve their efficiency and sustainability. All participants in a value chain were identified with the assistance of existing customers or Community-Based Organisations (CBOs). During the year under review, the Bank organised a financial literacy programme in Hettipola for members of the Sithamu Women’s Agriculture Association engaged in cultivation and livestock farming. Financial and technical support was extended to 532 tea growers attached to four tea societies in Bandarawela, Deniyaya and Gampola whilst four earth drilling machines and two tea harvester machines were donated to selected tea grower societies in the above region through In-kind Grant Initiative. This programme has previously benefitted traditional rice producers and farmers in Kokkadichcholai and Batticaloa, the dairy value chain of the Mullaitivu Livestock Breeders Cooperative Society, and a group of dairy farmers in Mulliyawalai.

Advancing card and cashless initiatives: À la card channels

Pushing the boundaries of customer service and experience through innovative products and services, the Bank enabled “Visa Direct” and “MasterCard Send” card-based fund transfer facilities for the first time in Sri Lanka. Debit and prepaid cardholders are enabled to transfer funds to any locally-issued Visa and MasterCard Debit, Credit, or Prepaid card through the Bank’s ATMs, CRMs, and Q+ Payment App, delivering enhancement of functionality and convenience. This fund transfer platform can be upgraded to facilitate businesses, government institutes, corporates, and merchants to do fund disbursements for various purposes.

Furthermore, the Bank became the first Sri Lankan Bank to introduce card acceptance through Android smartphones, allowing its merchants to conveniently and cost-effectively accept card payment transactions. The enabling of “Smart Phones” to accept Card payments interacting as a POS device branded as “Tap to Phone” allows merchants to conveniently and cost-effectively accept Card payment transactions using their mobile devices. This innovation has changed the landscape of the digital payment industry in Sri Lanka with the state-of-the-art low-cost technology, by converting any NFC-enabled Android smartphone into a payment acceptance terminal with utmost security.

In order to support the sustainability practices while safeguarding the environment, a novel feature was introduced replacing paper receipts with Digital receipts covering the ATM and CRM withdrawals. This feature is available to ComBank Cardholders when making a withdrawal from ComBank ATM/CRM, through transaction SMS with a link for a printable PDF digital receipt to their registered mobile number instead of disbursing paper receipts from ATM/CRM.

Trilingual presence: Tripartite inclusivity

The Bank in its service and product portfolios saw to the implementation of trilinguality to connect with customers from different cultural, religious, and ethnic backgrounds. An example of trilingual services deployment was seen with the launching of the Integrated Contact Centre in 2020 to serve its customers and stakeholders 24/7 and enabling customers to reach the Bank via multiple channels and languages for inquiries and assistance. Also, the Bank’s on-site customer service teams are equipped with trilingual proficiency to better serve the customer base.

The Bank’s website, now an indispensable tool for millions of customers and information seekers, has been re-launched as a trilingual resource, with a series of cutting-edge enhancements. A stand-out feature of the re-launched website is the option of browsing in the language a visitor is most comfortable in. The new and enhanced Commercial Bank corporate website has been launched with access to content in English, Sinhala and Tamil, an ultra-smooth interface with interactive multimedia material, enhanced navigation, experience-customisation, smarter search options and tools, and resources that make it extra user-friendly and informative.

Some of the banking products with a trilingual presence launched in 2022 are given below.

3. Leading through innovation

Digital strategy: A vista for convenience

The Bank remains committed to creating a digital culture, identifying digital initiatives, using integrated technologies, balancing brick and mortar vs digital channels, integrating legacy systems, conducting smart experiments, offering smart interactions, opening databases through APIs, upgrading business models, unlocking new revenue sources, and augmenting the digital experience of stakeholders. The Bank’s digital initiatives have continued to garner recognition through awards and accolades. The Bank was the largest facilitator of CEFT transactions in Sri Lanka with over 27 million transactions for the 12 months ended December 31, 2022. The Bank’s stakeholders have become more comfortable with the digital frontier, increasingly mastering the digital learning curve with a wide acceptance of digitalisation. Accordingly, the Bank’s digital banking retail customer base grew by 49% YoY, and its digital banking business customer base grew to over 43,000 users.

Table – 11: Investments in IT infrastructure

| Indicator/Year Rs. Mn. | 2022 | 2021 | 2020 | 2019 | 2018 |

| Investments in Hardware (Computer Equipment) | 2,440.880 | 434.054 | 505.742 | 567.689 | 1,034.115 |

| Investments in Software (Licenses etc.) | 2,218.024 | 768.047 | 409.322 | 387.432 | 333.181 |

| Total | 4,658.904 | 1,202.101 | 915.064 | 955.121 | 1,367.296 |

Table – 12: Migration to digital channels

| Indicator/Year | 2022 | 2021 | 2020 | 2019 |

| Number of existing customers migrated to online banking | 265,183 | 212,806 | 157,599 | 109,873 |

| New customer acquisition through digital channels | 9,539 | 12,491 | 16,327 | 14,957 |

Table – 13: Total financial transactions initiated through digital channels

| Indicator/Year | 2022 | 2021 | 2020 |

| Number of transactions (Total transactions without SLIPS/CEFTS) | 49,086,590 | 37,841,881 | 23,724,058 |

| Value of transactions (Rs. Bn.) (Total transactions without SLIPS/CEFTS) | 3,586.280 | 2,356.170 | 1,386.250 |

| % of customer transactions below Rs. 200,000 (%) | 94 | 92 | 97 |

| Growth in number of transactions (YoY) (Total transactions without SLIPS/CEFTS) (%) | 30 | 60 | 10 |

| Growth in value of transactions (YoY) (Total transactions without SLIPS/CEFTS) (%) | 52 | 70 | 22 |

Digital roadmap 2022 -2024: At the heart of the journey

Aligned with the Bank’s digital vision of building a digital economy where each customer is engaged at their level of techno literacy, the Bank’s digital roadmap is focused on retail customers encompassing products, services, processes, and touchpoints. The digital transformation for the next three years is driven by the following goals:

- Service transformation to achieve service excellence.

- Operational transformation to be more efficient and effective.

- Digital transformation to reaffirm digital leadership.

- Talent transformation to enhance performance.

Accordingly, the Bank continued to invest in redesigning its conventional banking processes as digital processes, integrating with other ecosystems, and upgrading internal systems to adapt to anticipated changes in the regulatory environment and risk management. Reskilling staff and attracting specialised talent, building partnerships, and developing its data capabilities continue to be focal areas as well.

Digital shelves 2022: Choices at your fingertips

The Bank identified opportunities to introduce new retail banking solutions to fill market gaps and implement proactive and remedial product changes to counter threats, competitor pressures, and other challenges. The retail arm of the Bank also supported the branch network by establishing partnerships for product value additions, sales drives, and cooperative campaigns, and by conducting marketing activities such as spot promotions and database marketing.

The series of digital products that were launched in 2022 include the Arunalu children’s savings account in foreign currency, 100, 200, 300, 400 days fixed deposit schemes, Forex Plus (FCY fixed deposit) scheme, and the Millionaire Investment Plan in foreign currency.

Product enhancements and changes were an integral aspect of the Bank in 2022. Product revamps in the Achiever Salary Savings Account and Udara Senior Citizen’s Account, a revised Isuru Minors’ Savings Plan and Millionaire Investment Plan, and the introduction of preferential interest benefits for Vibe Youth Savings Account holders when obtaining education Loans, were some of the key retail product changes during the year. The Bank entered into partnerships to offer value additions to its customers throughout the year. A special loan scheme was launched targeting “First Time Home Buyers & Builders”. Furthermore, in relation to leasing, the Bank launched a Discount Voucher Scheme partnering with leading automotive service providers, and dealers in the supply of spare parts and accessories. In addition, a feature called Loan Leads through WhatsApp banking provides customers the ability to apply for a Personal Loan, Home Loan, or a Leasing Facility through the ComBank WhatsApp Banking service.

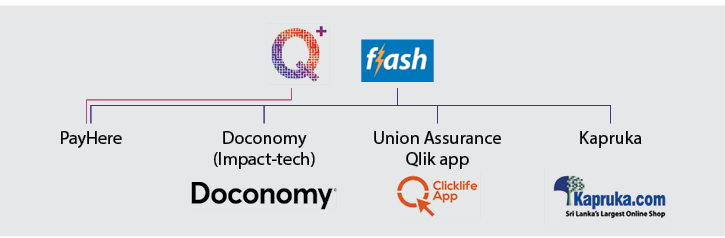

Flash toolkit: A future-friendly panacea

The winner of the award for the “Digital Banking Initiative of the Year” in Sri Lanka at the 2021 Asian Banking and Finance (ABF) awards, Flash is an all-in-one digital banking solution/toolkit that helps the customer manage lifestyle aspects by provisioning a payment portal for daily living and utilities, all under a unitary platform.

The Bank introduced two innovations to the Flash toolkit in 2022 fueled by the latest technology i.e., the introduction of wearable banking for the first time in Sri Lanka through Flash and the introduction of Digital KYC (Know Your Customer) for Flash new customer onboarding process.

This innovative wearable banking solution allows users to view their account balances and accept fund transfer requests directly from their Apple watches. In the future, the Bank plans to expand the functionality of wearable banking to include bill payments and own account transfers. To access this feature, Apple watch users simply need to download the Flash app to their watches through their iPhones, and they will be enabled to view their account balances and receive notifications for payment requests directly on their watches.

The Flash Digital Bank Account introduced a new video call identity verification feature that allows customers to open, activate, and operate an account without the need to visit a bank branch in person. This innovative feature allows for secure and convenient account management without the need for physical visits to the Bank. The unique Digital KYC process enables the Bank to complete the customer verification requirements remotely and activate the customer’s Flash account which allows customers to get full access to the app without visiting the Bank.

The “Loan against eFD,” was launched to offer the Flash customer to request a cash loan against an eFD opened under a Flash product. Upon approval, the funds are transferred to the Flash account and the customer is notified via SMS/in app notice.

The expanded Flash toolkit was also redefined by the following alliances that saw the introduction of four new cooperative products.

In the ensuing years, Flash is envisaged to expand further to include a new user interface with enhanced user experience, extend Flash for overseas Sri Lankan citizens, and enable a Flash Teens Version.

ComBank Digital: Swift and secure

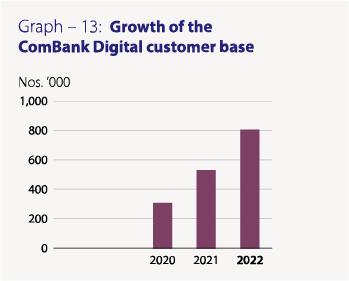

“ComBank Digital”, the single omnichannel digital banking platform is one of the top 5 financial apps in use in Sri Lanka. The platform provides seamless transitions across a range of devices including desktop computers, tablet computers, and mobile phones for ComBank Digital Customers. It consists of internationally recognised user security features with industry standards and a vast range of services. ComBank Digital has been enhanced further to serve the requirements of business users with enriched features and functionalities. During the year, the Bank’s ComBank Digital customer base grew by 51% YoY to over 800,000. The platform was launched in Bangladesh during the year.

ComBank Digital now enables payments to government authorities such as the Inland Revenue Department (IRD), Sri Lanka Ports Authority (SLPA) for cargo, vessel, and entry permit payments, Sri Lanka Customs, Employees’ Provident Fund (EPF), Employees’ Trust Fund (ETF), Import and Export Control Department (IECD), and the Board of Investment of Sri Lanka (BOI), providing its users with a convenient and secure platform.

The personal loan request feature on ComBank Digital makes it possible for customers to request a personal loan without visiting a bank branch. All correspondence is conducted via the user interface of the online platform, eradicating paperwork, and thereby promoting eco-friendly practices in addition to the convenience factor. This digital facility was adjudged the “Best Frictionless Credit Evaluation Initiative” in Sri Lanka by the Asian FinTech Academy (AFTA). The award was presented to the Bank at the “Asian Digital Finance Forum and Awards” at the Hilton Colombo in 2022, in recognition of the strides made by ComBank Digital to improve the digital banking experience for customers with enhanced functionality, convenience, and security.

State-of-the-art innovations: Efficiency internalised

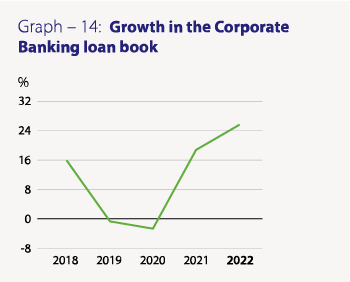

Through ongoing state-of-the-art innovation, the Corporate Banking arm enhanced customer experience during the year under review. The Introduction of the Customer Dash Board, Memorandum Circulation and Approval System (MCAS) workflow, and an EWS were some of the innovations of the year 2022.

The Customer Dash Board was developed and established during the year as a monitoring and analytical tool for the Relationship Managers and the management staff of the Department. The Dash Board provides portfolio details, product mixes, interest rate analysis, lending sector exposures, monthly trend analysis, non-performing advances, and overdue positions. MCAS workflow was introduced to replace the manual process of obtaining approvals which is cost-effective, time-saving and paperless. The Bank also developed a document tracking system to enhance internal efficiency which is currently deployed at the Trade Finance Division.

EWS models which are developed using data analytics techniques are expected to predict potential exposures showing signs of delinquency 9-12 months in advance. This provides the Lending Officers adequate lead time to attend to such warnings with appropriate and well-thought remedial measures.

Going forward, the Corporate Banking division hopes to deploy a Corporate Banking platform to ensure customer centricity with front end and back end capabilities cutting through all service and delivery points.

IT Road Map: Technology personified

According to the IT Road Map, moving from a traditional virtualised platform to an HCI platform (Hyper-Converged Infrastructure) was one of the key achievements completed during 2022 in terms of the Bank’s Data Center (DC) infrastructure. This facilitates the Bank to expedite the adoption of digitalisation and an IT-driven culture to secure its premier position in Sri Lanka's banking industry. The enhancements include automated capacity management and planning, performance monitoring and analytics, predictive DRS (Distributed Resource Scheduling) and DRS Management, proactive high availability (HA), and private Cloud-ready infrastructure.

The other noteworthy developments introduced during the year to build a robust back end digital process to enhance customer experience include the following:

- The Core Banking server infrastructure was upgraded to the state-of-the-art IBM POWER 10 technology with an investment of Rs. 1.2 Bn. This upgrade has enhanced the performance, security, and reliability of the core banking system. Furthermore, the Bank invested in Fiserv's latest Signature core banking platform that would augment the Bank's digital footprint, fostering more sectoral participation and a diversified customer base.

- A dedicated IT monitoring team was convened to provide, faster response and resolution for IT system issues and take proactive measures to increase the availability of IT services, 24x7.

- The operational efficiency and the service level agreements (SLA) were enhanced by setting up a Help Desk operating 365 days a year.

- The security infrastructure was enhanced by investment in a state-of-the-art security infrastructure with IPS upgrades, Perimeter Firewalls, and Active Directory, increasing the confidence and trust of customers and other stakeholders in the Bank.

- The digital receipt facility was enabled for ATM & CRM transactions which will enhance customer convenience, and reduce transaction charges and paper wastage.

- To increase Data Analytics and Machine Learning, the Bank launched three machine learning predictive analysis models (Transaction Analysis, Sentiment analysis, and Macroeconomic analysis) to identify and target potential borrowers for cross-selling and up-selling opportunities. Powered by a Big data platform, the system is implemented with Hadoop clustering for the first time in the history of the Banking industry in Sri Lanka. Technologies such as Spark, Airflow, Scoop, Python & Tableau are used for data extraction, analysis, automation, and visualisation.

- ComB HR mobile Application was launched to keep abreast of the mobile-savvy new generation of employees. As an initial step, this application was launched with features such as a staff contact directory, allowance details, staff profile, a reference guide containing the details of the products offered by the Bank, and news feeds. The app will be equipped with more features to enhance the value proposition offered to the staff members.

- The IT audit was completed in 2022, with the overall objective of examining and evaluating IT systems, architecture, and human resources against the recognised international standards and controls whilst enrolling business requirements in the digital space. The key focus areas of this project were maintaining critical system availability, strengthening IT governance and compliance, enhancing the structure, resources, and internal processes, assuring industry standard information security best practices and establishing architecture governance.

4. Operational excellence

Operationally resilient: Embodiment of grit

The Bank’s adaptability and operational resilience were tested in 2022. With COVID-19 being a significant disruption, the world embraced in 2020-22, a culture of remote work, increased virtual, technology-enabled operations, relaxed clocking hours, and a move towards net productivity models over a rigid clocking of time, had ripple effects on the Bank’s overall journey. In the face of manifold disruptions, the Bank had to break away from the traditional brick-and-mortar mindset, and adopt readymade time-tested systems, to offset the threats by being a fast learner of the “new normal” of a pandemic that derailed life globally.

It is said that to learn, we must first unlearn, and in that articulation, there is a sense of letting change have its candidacy to cultivate a bevy of new developments. Such developments include minimising face-to-face interactions, a surge in digital communicating apps and software, and a gradual diversification towards nurturing a remote workforce that changed the way employees work and do business.

The Bank made significant headway during the year under review in adapting to newer paradigm shifts brought on by the pandemic. Propelled by integrated thinking, the Bank effected customised acumen and future-friendly designs pulling the Bank to newer milestones, in firm control of its foreseeable and distant destinies.

As a well-oiled financial engine, the Bank ensured close coordination of functional divisions that synergistically ensured value creation. The banking operation of 2023 and beyond, hopes to continue in that same ethos, to scale the heights by the dualism of leveraging its strengths and being agile, to navigate the complex operating context.

The numerous awards and accolades garnered by the Bank bears testament to the strength, innovation and resilience of the Bank. Please refer the list of awards.

Key productivity and efficiency ratios depicting operational excellence is given below.

Table – 14: Productivity and efficiency ratios

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| Cost to Income ratio (Including taxes on financial services) (%) |

29.22 | 37.97 | 39.96 | 49.41 | 46.35 |

| Cost to Income ratio (Excluding taxes on financial services) (%) |

26.29 | 31.61 | 33.95 | 38.51 | 36.85 |

| Revenue per Employee (Rs. Mn.) | 53.787 | 31.720 | 29.605 | 29.377 | 27.462 |

| Profit per Branch (Rs. Mn.) | 79.480 | 82.251 | 57.050 | 59.320 | 61.557 |

| Profit per Employee (Rs. Mn.) | 4.485 | 4.654 | 3.238 | 3.363 | 3.490 |

A transformed working environment: Metamorphosis of enterprise

The Bank metamorphosed strategically in the dualities of financial intermediation and maturity transformation in 2022, to ensure its readiness to offer uninterrupted services to its stakeholders through the implementation of the Business Continuity Management (BCM) framework. The Bank’s continued to prioritise the human factor, deliver its services to customers, and ensure the health and well-being of the employees, whilst complying with regulatory requirements, and adhering to good governance principles, at all times. The key principles of the BCM include,

- Support the Bank’s core banking systems and assuring that all mechanisms and processes are marshalled by the Bank’s guiding principles to ensure service continuity.

- Ensure availability of the systemically important payments and securities settlement systems by meeting the predefined service levels after a disruption.

- Minimise the financial, legal, and other operational risk associated with disruption of operations or failures.

- Protect human life and ensure minimal exposure to hazards and dangers within the Bank’s ecosystem.

- Safeguard the Bank’s image and reputation.

- Minimise the impact of disruption and ensure that maximum resources were streamlined to resume normal operations by implementing effective incident and crisis management and business continuity.

Risk aversion and management: The safety net

The Bank continued to effectively manage its risk appetite and risk tolerance, especially in the context of the challenges faced by the banking sector. The Bank continued to focus on preserving the quality of the loan book, managing interest rates, and liquidity while improving compliance to minimise reputational risk.

Conducting risk-control self-assessment exercises, regular evaluations of risk management processes and tools, and probing the Key Risk Indicators (KRIs) in relation to the traffic of risks were integrated into the culture of the Bank. The Bank’s compliance with relevant laws, regulatory guidelines, and internal controls in all areas of the business operations, was pragmatic in the effective management of risks. Key risk areas included credit, operational market, liquidity, IT, and other risks that can have negative bearings on the sustained growth of the Bank, affecting both governance and operations.

For 2023, the compass is pointing towards prudent, cohesive, and continued growth and strategic leveraging of key risks that would play an important role in catalysing cautious prudence into improved confidence. In particular, the Bank will focus on managing emerging risks - such as model risk, conduct risk, bribery risk, and more to create sustainable value for its stakeholders.

The transformation of the banking model: Metamorphosis of core elements

The banking business model is undergoing a radical shift, driven by new competition from expanding utility companies and emerging Fintechs, the quantum leaps of blockchain and cryptocurrencies powered by digitisation and convenience, and mounting regulation and compliance pressures. Furthermore, the banking industry is facing a new era that requires banks to future-proof their risk exposures without having any historical evidence or data on how to predict or tackle the risk, with a limited window of opportunity to adapt and respond to emerging scenarios.

Technology is blurring the contours of the banking industry, a risk that mandatorily demands an upsurge of digital products, which require upskilling in digital literacy of the front end of customer interfaces and internally, employees requiring stronger proficiency in tailormade systems. The Bank reviewed and revised the disaster recovery plans while managing the footprint of COVID-19 and associated phenomena such as long COVID and co-morbidities that has a bearing on the productivity and health of the employees.

Resources were allocated to manage the diverse risks whilst nurturing a positive risk culture across the Bank, top-down, with the Board of Directors, Corporate Management, and the Board Integrated Risk Management Committee setting strong precedence. This included the use of EWS with a greater emphasis on real-time data and machine learning models and the gradual restoration of Foreign Currency Reserves to its former strengths.

Remuneration and job security: Shielding from the perfect storm

In a climate of increased financial toll, the Bank strived to ensure that the employees were endowed with continuing remuneration on par or over industry standards. This enabled safeguarding the employees from the stresses of the pandemic. For more details, please refer “Remuneration and Job Security: Generosity Personified”.

Collective bargaining: The dialogues

Demonstrating a hand-in-hand partnership with Commercial Bank Employees Union (CBEU), the Bank signed an agreement with CBEU in 2021 for a further 3 years. During the year under review, the Bank continued to engage in cordial relations with the CBEU, with negotiations fueling dialogue between the two entities, provisioning two-way rewards to the Bank as well as the employee union.

Training and development of staff: Stepping up

The Bank engaged in a range of training and development schemes to ensure that the employees are custodians of lifelong learning and strategic self-development that can be vehicles of self-actualisation. The above is narrated in section on Staff Training: Learning Curves.

The Bank believes that upholding recognised standards and principles for labour practices, human rights and occupational health and safety is essential to remain productive. Especially in a challenging context, it was important to prevent burnout and exhaustion and bolster morale, and provide employees with an environment where they could flourish and drive the success of the Bank. Even through the difficult circumstances, camaraderie and team spirit of the staff remained strong and their productivity remained high and consistent.