Operating Environment

Material Matters

As the COVID-19 pandemic tailed off, newer trends and developments surfaced with multiple influences on the banking operations. The acceleration of the demand for digital banking prompted the Bank to further augment its digital offering around customer value streams encompassing the entire customer journey from beginning to end. In particular, the wave of digital products that were introduced since 2020, stood as key innovations, helping in the transformation of a “footfalls” culture into a shelf of digital products at the stakeholders’ fingertips. While ushering timely change, the Bank helped stakeholders not just to migrate to digital channels, but to adopt environmentally-responsible practices in their business operations focused on reducing the carbon footprint. The Bank emerged from the pandemic into a whole new era of green precedents and products, where procurements and lending were compliant to both the internal and external taxonomies of sustainable banking. Creativity was a standout livewire that kept the Bank’s product offering avant garde, heralding mass digitalisation of exterior channels and automation of internal processes.

The Bank’s resilience was second to none. Being agile to the metamorphic changes in technology, demographics, and preferences of the stakeholders, the Bank adapted nimbly to the exterior environment. As a champion of technology, the Bank continued to strengthen the technological and financial literacy of the customers by assisting them in all banking matters throughout their journeys with the Bank. Trilingual presence in both over-the-counter and call center interfaces was a resounding success in the retention and expansion of the customer base. The Bank was also vigilant on global trends, and kept abreast of the latest initiatives, technologies, disruptions and novelties that shaped the year 2022. While market and credit risks were internalised into the ethos and workmanship of the Bank’s financial dealings, the Bank kept a watchful eye over its financial cushions, always staying adequately stocked with liquidity while maintaining capital buffers, embarking on farsighted provisioning, in a time of financial crises.

The major disruptions of 2022 were of multiple origins. Due to a plurality of factors, including downgrading of the sovereign credit rating, decline in worker remittances, drop in tourist arrivals, diminishing forex reserves, issues related to debt sustainability, and sharp depreciation of the Rupee, amongst others, Sri Lanka was faced with a bleak and austere 2022. In such a milieu, astute and forward-thinking measures were the need of the moment. Resilience was about staying ahead of disruptions, to stay relevant as a modern outfit that is technology-empowered, digitally road-mapped, automation-friendly, and forward-thinking, without losing the fundamental values the now post-centenarian Bank was originally built on.

In order to help identify material topics, adapt the Bank’s strategy to face the “new normal”, and play a significant role in shaping the recovery, the Bank analysed its external environment to identify matters arising from changes that were brought forth by the various developments in the political, economic, social, technological, environmental, and legal/regulatory spheres in the recent past that were relevant to key stakeholder groups, as given below:

Figure – 06: Matters relevant to the key stakeholder groups

| Political | Economic | Social | Technological | Environmental | Legal/Regulatory | ||||||||||

Investors  |

1 | Lack of desired level of policy consistency | 2 | Economic slowdown | 3 | Growing influence of social media |

4 | Unorthodox competition and financial disintermediation | 5 | New regulations, compliance requirements, and directives | |||||

| 6 | Lack of desired level of transparency and accountability | 7 | Depreciating currencies against USD | 8 | Demand for non-financial information and long termism | 9 | Compliance with Basel requirements | ||||||||

| 10 | Downgrading of the Sovereign rating and its cascading effect on the Banking industry | 11 | Demand for more transparency and accountability | 12 | Higher regulatory capital as a D-SIB | ||||||||||

| 13 | High CAPEX requirements | 14 | New Banking Act | ||||||||||||

Customers  |

15 | Asset growth and asset quality |

16 | Changing customer expectations | 17 | Migration towards digital platforms | 18 | Compliance requirements and regulations such as FATCA1, GDPR2, and BEPS3 | |||||||

| 19 | Import restrictions | 20 | Cybersecurity Threats | ||||||||||||

Employees  |

21 | Need to enhance productivity | 22 | Talent management | 23 | Need to reskill staff with technological advancements | |||||||||

| 24 | Health and Safety | 25 | New working cultures | ||||||||||||

Society and environment  |

26 | Geopolitical conflicts | 27 | Declining worker remittances | 28 | Need to commit to Sustainable Development Goals (SDGs) | 29 | Increasing frequency and magnitude of natural disasters and poor disaster preparedness | |||||||

| 30 | Corruption | 31 | Declining global competitiveness of Sri Lanka | 32 | Increasing conflicts | 33 | Increasing demand for green banking and green lending | ||||||||

| 34 | Pandemics hampering world trade and economy | 35 | Increasing drug pedaling and drug and alcohol addiction | 36 | Climate change | ||||||||||

| 37 | Being socially responsible | ||||||||||||||

Business partners |

38 | Partnerships for goals through a more collaborative approach | 39 | New technological advances such as AI, Robotics, blockchain | |||||||||||

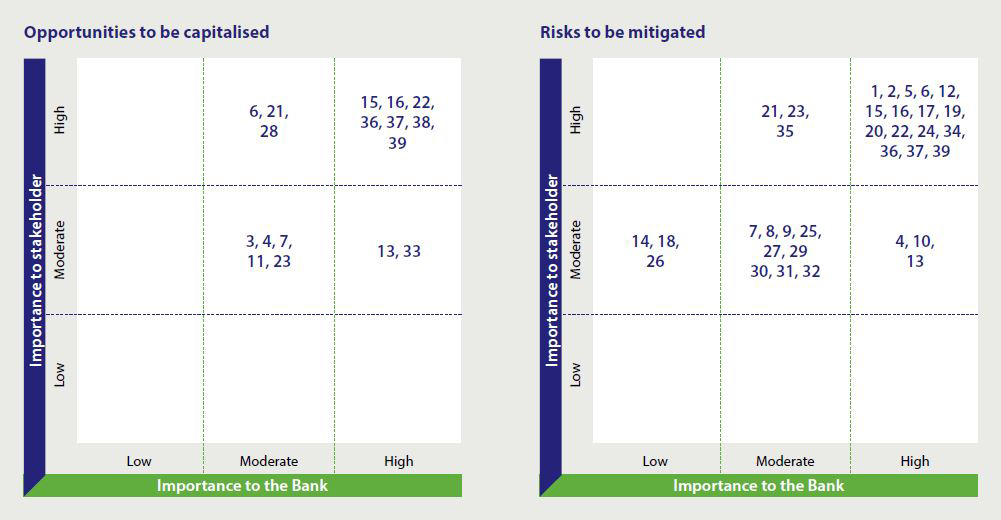

Materiality matrix

Management approach

The Bank has the best interest of all the stakeholders at heart and therefore, respects mutuality and shared value when delivering value to and deriving value from them that lead to value creation.

In the process, the Bank manages its material topics through its strategic planning process. This entails assigning responsibility to the heads of the relevant divisions of the Bank and allocating the required resources based on the significance of each material topic towards achieving the aforementioned strategic imperatives. The Bank has embedded goals and targets, where appropriate, into the KPIs of the Key Management Personnel (KMP) and are reviewed on a regular basis, to ensure achievement of its objectives with regard to its material topics.

Many policies have been put in place to guide the staff to conduct activities in a responsible, transparent, and ethical manner in managing the material topics. The Board of Directors has duly adopted these policies, which are reviewed at predetermined intervals to maintain them current to reflect the changing conditions. The Integrated Risk Management Department (IRMD) keeps a track of timely revisions to these policies and reports its observations to the Board Integrated Risk Management Committee (BIRMC).

Where relevant, grievance mechanisms have been established with responsibility assigned to the relevant divisional heads to manage, address and resolve grievances. The Bank’s lending to its customers and dealings with its business partners are screened for social and environmental aspects.

To ensure adherence to internal controls, policies, and procedures established to accomplish the objectives of material topics, internal and external audits and verifications are conducted periodically, and findings are reported to the Board of Directors and/or to the relevant Management Committees for information and corrective action, where necessary.

Overall risk profile of the Bank depicted by its rating and the awards and accolades that the Bank has secured over the years, clearly demonstrate the effectiveness of this management approach.

Material topics, risks, opportunities, how we manage and GRI disclosures

The Bank has identified matters mapped into the blocks relating to the high importance to stakeholder and high and medium importance to the Bank under both opportunities to be capitalised and risks to be managed in the Materiality Matrix shown above as material topics.

Table – 04: Material topics, risks, opportunities, how we manage and GRI disclosures

| Material matters | Risks | Opportunities | How we manage | GRI disclosure |

| Policy inconsistency 1 |

Difficulties encountered in the process of planning and budgeting and risk of being unable to comply with regulatory requirements, leading to strategic risks. | Increasing the stress levels of the parameters used for and frequency of stress testing. Frequently reviewing strategies and goals against changes in the external environment | GRI 201: Economic Performance GRI 207: Tax | |

| Economic slowdown 2 |

Stifled business growth affecting value creation and resulting disappointment among the stakeholders. | Being prepared to meet the pent up demand that could arise when the situation comes back to normalcy. | Being alert to the developments and maintaining fundamentals to exploit opportunities when they come. | GRI 201: Economic Performance |

| New regulations, compliance requirements, and directives 5 and 12 |

Increased costs in implementation, modification, and monitoring of process and the risk of not being compliant. | Good governance is the bedrock of a sustainable business and helps boost stakeholder confidence. | Bank is committed to being compliant to the letter and spirit of rules and regulations and believes in commitment to good governance provides a strong footing for sustainable growth. Please refer section on “Annual Corporate Governance Report”. | GRI 205:

Anti-corruption

GRI 206: Anti-competitive Behaviour |

| Transparency and accountability 6 |

Non-disclosure of adequate information may give rise to reputation risks and regulatory pressures. Increased demand for forward looking strategic direction by investors over conventional reporting of past performance. | Transparency breeds extra assurance on the Bank, creates trust, leverages faith that will be seen in an upsurge of stakeholder engagement. It will also help reduce risks of unwarranted suspicion and help achieve faster resolution of issues and reputation related risks. | Bank’s approach on transparency and accountability is discussed in detail on the section on “Annual Corporate Governance Report”. | GRI 205: Anti-corruption GRI 207: Tax |

| Downgrading of sovereign rating 12 |

Reduction of international trade transaction volumes and hampers the ability to raise foreign currency in the international market | Healthy mix of foreign currency portfolios and Bank's regional presence supporting foreign currency liquidity supports Bank's ability to sustain its foreign currency transactions. | Bank's strength in the foreign currency mix in the balance sheet, built over the years and our regional presence has supported sustain our foreign currency operations. the section “Managing and Funding Liquidity” provides as insight how the Bank managed the impacts of this material aspect. | GRI 201: Economic Performance |

| Asset growth and asset quality 15 |

As a financial intermediary, Bank’s value creation depends heavily on its ability to gear its capital in terms of assets and the quality of those assets. Inability to grow assets and deterioration in asset quality will lead to regulatory issues, stifled business growth and disappointment of stakeholders. | Growing the asset base and improving asset quality by strengthening credit evaluation and post disbursement monitoring mechanisms, using predictive capabilities. | The Bank implemented an Early Warning Signals system with predictive capabilities that can possible deterioration in asset quality 9-12 months in advance. | GRI 201: Economic Performance |

| Changing customer expectations 16 |

Customers, millennial in particular tend to value simplicity, convenience and experience above everything else in their interactions with the Bank, creating a risk for the Bank in maintaining customer loyalty by providing its services in a conventional manner. | Augmenting customer experience to capture the new age customers by investing in state-of-the-art technologies to replace legacy systems and reskilling staff for the digital age. | Investing in new technologies, implementing the Digital Road Map and continuous development of staff knowledge on emerging technologies. | GRI 203: Indirect Economic Impacts |

| Migration towards digital platforms 17 and 39 |

Failure to migrate to digital platforms and deploy new technologies such as AI, Robotics, blockchain etc. will affect customer service and their experience as well as operational efficiency. | Migration to digital platforms and deploying new technologies such as AI, Robotics, blockchain etc . will augment customer service and their experience as well as operational efficiency. | The Bank has introduced many digital platforms and apps to suit the divergent customer base of the Bank and is gradually introducing new technologies for its internal operations. | GRI 203: Indirect Economic Impacts |

| Import restrictions 19 |

Curtailed business opportunities and less fee-based income from capital friendly international trade related businesses. | Gearing to exploit the pent up demand that may come up when restrictions are relaxed. | Minimising the impact by canvassing customers from industries / sectors who are not affected by the import restrictions. Diversifying the business operations. | GRI 201: Economic Performance |

| Cyber security 20 | Cyber threats continue to increase globally and the need to protect the integrity and privacy of data becoming important than ever before. The pandemic has fuelled the risk of cyber attacks and thefts. | Having a robust cyber security programme boosts customer confidence in embracing and using digital platform and provides a distinctive advantage over competition in digital banking space. | A high importance is placed on this critical aspect and is always on the toes. Internationally recognised certifications we hold vets the robustness in our security systems. For more details please refer the section “IT Risk” in Risk Governance and Management report. | GRI 418: Customer Privacy |

| Productivity 21 |

With the conventional business model, the profitability of the financial services industry has been declining globally over the past several decades. Productivity is an important aspect that will help to improve profitability. Failure to adopt mechanisms such as automation and digitalisation will make the Bank less attractive to most of the stakeholders. | Enhancing profitability through investing in automation and digitalisation to enhance operational efficiency and improve profitability and attractiveness of the Bank to them. | Investing in new technologies, implementing the Digital Road Map and continuous development of staff focussing on digital channels to facilitate the entire customer journey. | GRI 203: Indirect Economic Impacts |

| Talent management 22 |

Among the risks brought about by the pandemic and the aftermaths of the political and economic unrest are the high staff attrition, health and safety of the workforce, sustaining critical operations, sudden adjustments in to new working conditions top the list. Staff retention and recruitment becoming more challenging. | Adoption of digital means for remote working results in enhancing technology related skills and prompt rethinking of working conditions that may improve work-life balance and reduction in costs. | The Bank has given utmost priority when it comes to investing in employee training and development and placing safety of employees first by providing a safe working environment. Deviating from the conventional practices, the Bank is successfully experimenting newer methods and levels to recruit staff such as recruiting more Management Training, recruiting A/L students awaiting results as banking interns, creating new categories of employment for certain specialised categories of staff such as IT staff. For more details please refer section “Operational Excellence” in the section on Sustainable banking – Value creation. | GRI 404: Training and Education GRI 405: Diversity and Equal Opportunity GRI 403: Occupational Health and Safety |

| Need to reskill employees 23 |

The Bank being unable to meet the stakeholder expectations, millennial customers in particular, due to the staff not being reskilled to keep abreast with the latest technologies. | Proper reskilling of staff and helping and encouraging them to keep abreast with the latest technologies will help to delight customers and create “moments of truth”. | Continuous training and development of staff and incentivising them to keep abreast with technologies used in the Bank. | GRI 401: Employment |

| Health and safety 24 |

Inability to ensure health and safety of staff will affect their work life balance and productivity and operational efficiency of the Bank. It may also lead to reputational risk. |

Ensuring health and safety of staff will help the Bank to improve its efficiency of operations, productivity and profitability. | Promoting the importance of work life balance, assigning to work places closer to the homes of staff members, providing medical and transport facilities at the expense of the Bank during COVID-19 outbreak and reimbursing medical expenses. | GRI 401: Employment GRI 403: Occupational Health and Safety |

| Need to commit to SDGs 28 |

As a national bank, failure to commit and work towards UN Sustainable Development Goals will seriously affect the sustainability of the banking operations and also cause reputational risk. | Commitment to UN Sustainable Development Goals will improve the sustainability of the banking operations and minimise reputational risk. This also makes the Bank's business model future-ready | Bank is explicitly committed and working towards 7 out of the 17 UN Sustainable Development Goals. Strategic initiatives in this regard are stemming from the Bank’s Sustainability Framework and are built into the strategy. | GRI 203: Indirect Economic Impacts |

| Pandemics affecting global trade and economies 34 |

Failure to detect instances of money laundering and related compliance and reputational risks. Also, drug and alcohol addicts can cause an increase in security related risks. | Compliance with all the applicable rules and regulations. Continuous strengthening of systems and procedures relating to detection and prevention of the use of the Bank for money laundering operations. | GRI 205: Anti-corruption |

|

| Drug pedalling and drug and alcohol addiction 35 |

Stifled business growth, curtailed business opportunities and less fee-based income from capital friendly international trade related businesses affecting value creation and resulting disappointment among the stakeholders. | Diversifying the business into industries and sectors that are less likely to be affected. | GRI 201: Economic Performance | |

| Climate Change 36 |

Increasing frequency and magnitude of natural disasters may affect infrastructure, banking operations, business growth, operating costs, asset quality, and pause reputational risks. | Responsible lending through Social and Environment screening may help reduce reputational risks and maintain asset quality. | Though the Bank’s own footprint is minimal, it endeavours to minimise same through adopting green processes, moving to green buildings and generating solar energy for it operations. However, the Bank could make a bigger impact through its lending to renewal energy generation, greening of processes, and screening for environmental impacts on businesses we lend to. Further, moving towards climate change mitigation procedures, such as reforestation with saplings, remote and hybrid work options lessening the commuting-dependent emissions are also helpful in this regard. How we do this is detailed in the section on “Climate Position Statement” in the section on Responsible organisation – Shared value. | GRI 302: Energy GRI 305: Emission |

| Being socially responsible 37 |

The world, increasingly ideological, will mandate that the Bank focuses on diversity factor to ensure that social justice, inclusivity and stakeholder welfare as apex issues. | Collaboration with Fin-Tech could open up new avenues to reach untapped markets and evolve alongside changing customer expectations. Advancement in new technologies such as Artificial Intelligence, Robotics, and Block Chain could be used to boost operational excellence. | We believe in sharing the value created with the society we operate. Hence, the Bank has set up a CSR Trust for undertaking projects for improving the quality of education, health, culture & heritage, and preservation of environment. Please refer section “Community Sustainability". | GRI 203: Indirect Economic Impacts |

| Partnerships for goals 38 |

Interruption to critical services could disrupt smooth execution of the Bank’s operations. Unorthodox competition, financial disintermediation, and failure to collaborate may threaten the conventional business model. | Increasing awareness and tendency towards renewable energy and greening of buildings and processes bring about green financing opportunities. Initiatives in countering impacts of carbon emission. Adopting a collaborative approach to co-create and offer products and services. | The Bank’s continued it efforts on building win-win partnerships and constantly seek for avenues to leverage evolving new technologies for the development of our own products, services, and delivery, described more in section on “Leading through Innovation” in the section on Sustainable banking – Value creation. |

GRI 206: Anti-competitive Behaviour |