The Board acknowledges that transparency and accountability are critical to achieving a high-quality governance mechanism that empowers the stakeholders, especially given the role played by the Bank as a financial intermediary.

Prof A K W Jayawardane

Chairman

Chairman’s Message

In a world that is contracting in its virtual and physical landscape – thus the Global Village concept; there is an unprecedented footprint of change on past brick and mortar ecosystems, now faced with a barrage of intrusions as well as emerging new markets. Ensuring competitiveness in such a changing and challenging global scenario is mandatory for growth. Heightened competition from both conventional players and new entrants such as fintechs; the increasingly capital-intensive nature of the business; rapid evolution of cutting edge and innovative technologies; demographic and generational changes; and ever tightening regulations have redimensionalised the banking industry. In this contemporary context, the financial services industry faces unprecedented challenges in scaling up operations.

The Bank is entrusted to be an ethical value creator. In that binding commitment, the Bank has to play by the rules and codes of ethics that form the core model of transparency not just as a good practice, but epitomising the ethical foundation - the twin pillars of financial intermediation and maturity transformation. Such an environment exerts even greater pressure on the industry to practice ensuring greater accountability, transparency, good governance, and sound financial and risk management to all their stakeholders while maintaining sustainable operations.

Accountability and prevention of corruption is possible only through implicit transparency. Accountability and transparency go hand in hand; the latter in fact enables accountability. The Board acknowledges that transparency and accountability are critical to achieving a high-quality governance mechanism that empowers the stakeholders, especially given the role played by the Bank as a financial intermediary.

In its core stewardship role, the Board has the ultimate accountability to the Bank’s stakeholders for the activities and performance of the Group. We are deeply conscious of our role in fulfilling the expectations of our stakeholders and of our responsibility to report to them on how we are meeting – and plan to continue reciprocating – those expectations. The Board adopts a strategic focus to ensure value creation over the short, medium and long term and takes responsibility for the consequences of the Bank’s actions and the resultant performance. The Board also keeps a tab on the actions and performance by timely disclosures including those made in this Integrated Annual Report, to ensure the continuity of transparency across its functional areas.

This requires implicit clarity as to who is responsible for what and to whom at all levels across the Group. In this regard, the Bank has established a number of committees at the Board as well as at the Executive level as elaborated in this Governance Report. These hardwired committees are guided by the relevant directions/guidelines of the regulators, and a number of Board-approved governing documents such as policies, frameworks, terms of reference, and charters, which are reviewed and approved by the Board at least annually. Similar Board-level as well as Executive-level committees have been established – as required – in the subsidiaries and the associate, too, showcasing the Bank’s commitment to the Group.

Besides the governing documents upholding Board’s roles and responsibilities, Board oversight on reporting, disclosures on related party transactions, performance evaluation and reward structures, and KPIs that target long-term sustainability, are other supporting practices that promote accountability and transparency.

During the year under review, the Bank introduced a new Conduct Policy and reviewed and updated the Anti-Bribery and Anti-Corruption Policy (https://www.combank.lk/info/file/91/anti-bribery-and-anti-corruption-policy) to further enhance our commitment to “best conduct” principles, which together with the Code of Ethics and the Whistleblowers’ Charter encourage all staff members at all levels to be ethical and accountable in their dealings. While acknowledging and guided by the need to maintain confidentiality, the precedents, policies and products that require timely disclosures are accessible through the intranet and the Bank’s website, as appropriate.

Achieving transparency is a function of information disclosure, both financial and non-financial, about the activities, performance and governance of the Group – and ensuring that this information is accurate, complete, and made available in a timely fashion to the stakeholders. In order to enhance accountability and uphold transparency, the Bank takes into account materiality, completeness, accuracy, balance, clarity, comparability and reliability when reporting on its performance. Assurance certificates obtained by the Bank on its financials, internal controls, sustainability, integrated reporting, and GRI indicators, etc. further corroborate the Bank’s own efforts to be a clear contender in both internal and external processes that require third party accreditation.

The publication of this Integrated Annual Report, which includes extensive voluntary disclosures that go beyond compliance requirements, is a clear demonstration of our accountability to the stakeholders. Guided by the new Sustainability Framework adopted during the year, we have been gradually expanding our focus and disclosures on environmental, social and governance-related aspects, to showcase in particular that the CSR Trust of the Bank envisages the social and environmental conscience as a pillar by itself, one not just of holistic sustainability but also a benefactor of corporate empathy.

The Bank is aware that in addition to its financial performance, the overall efficacy of its long-term value creation will be judged by its contribution to the society and the environment. In our view, these are mutually inclusive aspects, and are equally important components in a comprehensive definition of sustainability. A profitable operation is a precondition for sustainability, and in such a bearing, the Bank sustains its financial portfolios well replenished to empower the CSR activities that trickle over to the palms, places, and plates of the most impoverished and the needy. These two dimensions are symbiotically-dependent such that both needs to be present for an enterprise to be sustainable. The Bank continues to renew its “license” to operate within a community, to the betterment of those who are physiologically insecure, financially deprived, and burdened with resource poverties.

Given that the Bank conducts its operations with the best interests of all the stakeholders at heart and it is backed by exemplary governance practices, as elaborated in this Corporate Governance Report, the Board of Directors is highly confident about the ability to sustain the Bank’s operations into the foreseeable future. Our actions will not be one of economising, but one that works on the guardianship of good practice principles written in the law, and de facto ones that are practiced consciously in the market place.

The Bank consolidates the financial aspirations of its stakeholders, while always being a benefactor of grassroots communities, and in that striking dualism of caring for its dependants and protecting the marginalised, the Bank ensures the human touch over quarterly windfalls.

Prof A K W Jayawardane

Chairman

Colombo

February 24, 2023

How we govern (Principles D.5 and D.6)1

As per the disclosure requirements of the Banking Act Direction No. 11 of 2007 on Corporate Governance (the Direction), in the section on Governance and Risk Management of this Report elaborate the structure, overarching principles, and elements of the Bank’s corporate governance framework. In addition, the Bank has complied with the principles enumerated in the Code of Best Practice on Corporate Governance – 2017 (the Code) issued by CA Sri Lanka.

The External Auditors of the Bank, Messrs Ernst & Young have submitted their Assurance Statement to the Central Bank of Sri Lanka (CBSL), following their review of the Bank’s compliance in line with the Direction.

The extent of compliance in line with the Direction is disclosed in Annex 1.1, while compliance with the Code is presented in Annex 1.2. Furthermore, the Bank has complied with all the disclosure requirements under the prescribed format issued by the CBSL for the publication of Annual Financial Statements, and a comprehensive disclosure statement thereon is given in Annex 1.3.

As the Bank is fully compliant with all the applicable requirements of the Direction, the Colombo Stock Exchange (CSE) has exempted the Bank from the disclosure of compliance with the regulations stipulated in Section 7.10 of the Continuing Listing Requirements on Corporate Governance.

Bank’s approach to governance

As the Bank holds the fiduciary responsibility of accepting and deploying vast sums of uncollateralised public funds, the importance of maintaining public trust and confidence for its long-term success and sustainability cannot be overemphasised. To this end, the Bank considers exemplary conduct on the part of all its employees as essential to good governance, be it from the Board of Directors at the highest governing body and the members of Corporate Management, to the Senior Management and the staff at the most junior level. Accordingly, the Bank has put in place a system of good corporate governance - the system of rules, practices, and processes that guides corporate behaviour ensuring a disciplined approach to decision-making and execution with the interests of all stakeholders at heart. This system has been the bedrock of the Bank of its existence for over 100 years and sustainable value creation.

At Commercial Bank, good corporate governance is not limited to legal and regulatory requirements alone but is viewed as a collective responsibility that serves as the foundation for financial integrity, sustainable value creation, and investor confidence. While it is a strong and highly effective risk management tool, it simultaneously paves the way for the Bank to exploit opportunities. Given this huge responsibility, the Bank has an unwavering commitment to good corporate governance and conducts its affairs with utmost intellectual honesty, integrity, and diligence whilst being mindful of its obligations to society and the environment. This tone is set at the topmost echelons of the Bank’s Corporate governance structure and echoes through the entire work culture at the Bank.

While the commitment to good corporate governance has been in place for over a century, the underlying framework is regularly reviewed and updated to be in line with the evolving regulations and best practices. The framework has consistently and successfully guided the Board, Board Committees, Management, Management Committees, and staff in performing their stewardship roles. This framework is underpinned by the governance principles of leadership, integrity, effectiveness, accountability, transparency, sustainability, and shareholder engagement. These principles guide the Bank's Management in all its decisions relating to Board oversight, delegation of authority, division of responsibilities, resource allocation, risk management, compliance, performance appraisal and compensation, related party transactions, and financial reporting. The fact that the Bank is the most awarded bank in Sri Lanka bears testimony to its commitment to good corporate governance (Refer for the details of awards and accolades won by the Bank during the year under review).

Objectives of the Bank’s Corporate Governance System

As the largest private sector bank and the third largest bank in Sri Lanka, Commercial Bank touches the lives of millions of people in various capacities, and these stakeholders in turn have high expectations of their interactions with the Bank. Given that this trust and confidence are imperative for the long-term success of the Bank, the Corporate Governance system has been designed to ensure the following as envisaged in its Business Model:

- Providing adequate oversight on Management to ensure due diligence on key decisions and implementation of strategies as intended

- Establishing clear ownership and accountability on key and emerging risks

- Maintaining efficient systems and processes to speedily identify, assess, and escalate issues, incidents, and risks

- Providing efficient decision-making for timely and effective outcomes to achieve expected results

- Ensuring business and support service functions are sufficiently resourced with the required competencies and maturity

- Ensuring the remuneration framework is properly aligned with the long-term success of the Bank

- Ensuring activities comply with policies, laws, regulations, and ethical standards both to the letter and spirit

- Ensuring assets are safeguarded

- Guiding the Bank and its Group companies to be more stable, resilient, and future-ready

- Creating value sustainably for all stakeholders over the short, medium, and long-term

To achieve the objectives stated above, the Board has ensured the following:

- Clearly demarcating and distributing the roles and responsibilities among the Board, Board Committees, Management, and Management Committees, with the approved charters and Terms of Reference reviewed annually

- Establishing clear reporting lines and frequency of reporting

- Taking into consideration the legitimate needs, interests, and expectations of all the stakeholders

- Upholding the highest degree of fairness, transparency, and accountability

- Setting out principles for countering bribery and corruption and the management of bribery and corruption risk through the adoption of an Anti-Bribery and Anti-Corruption Policy and communicating same to all staff clearly indicating the Bank’s stance on zero tolerance for non-compliance

- Adopting a Group Conduct Risk Management Policy Framework

- Aligning remuneration to performance, based on accurate job descriptions, agreed on KPIs and clear communication of expectations from the employees

- Minimising negative externalities to society and the environment

- Living by the claims made and values associated with the Bank’s brand reputation

- Establishing a Sustainability Framework to operationalise sustainable banking, responsible organisation, and community sustainability

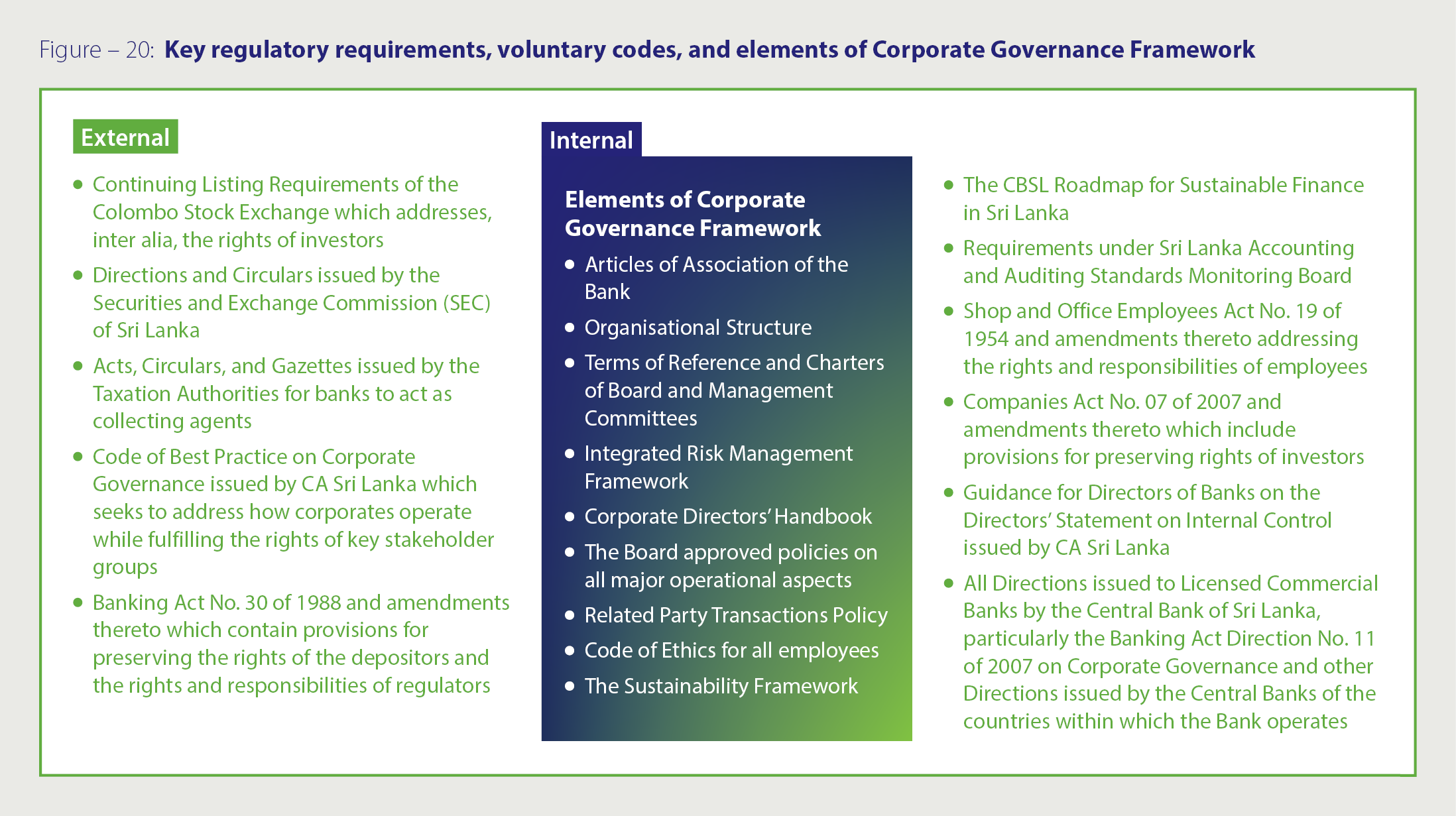

The key regulatory requirements and voluntary codes relevant to the Bank and elements of its Corporate Governance Framework are depicted in Figure 20 below.

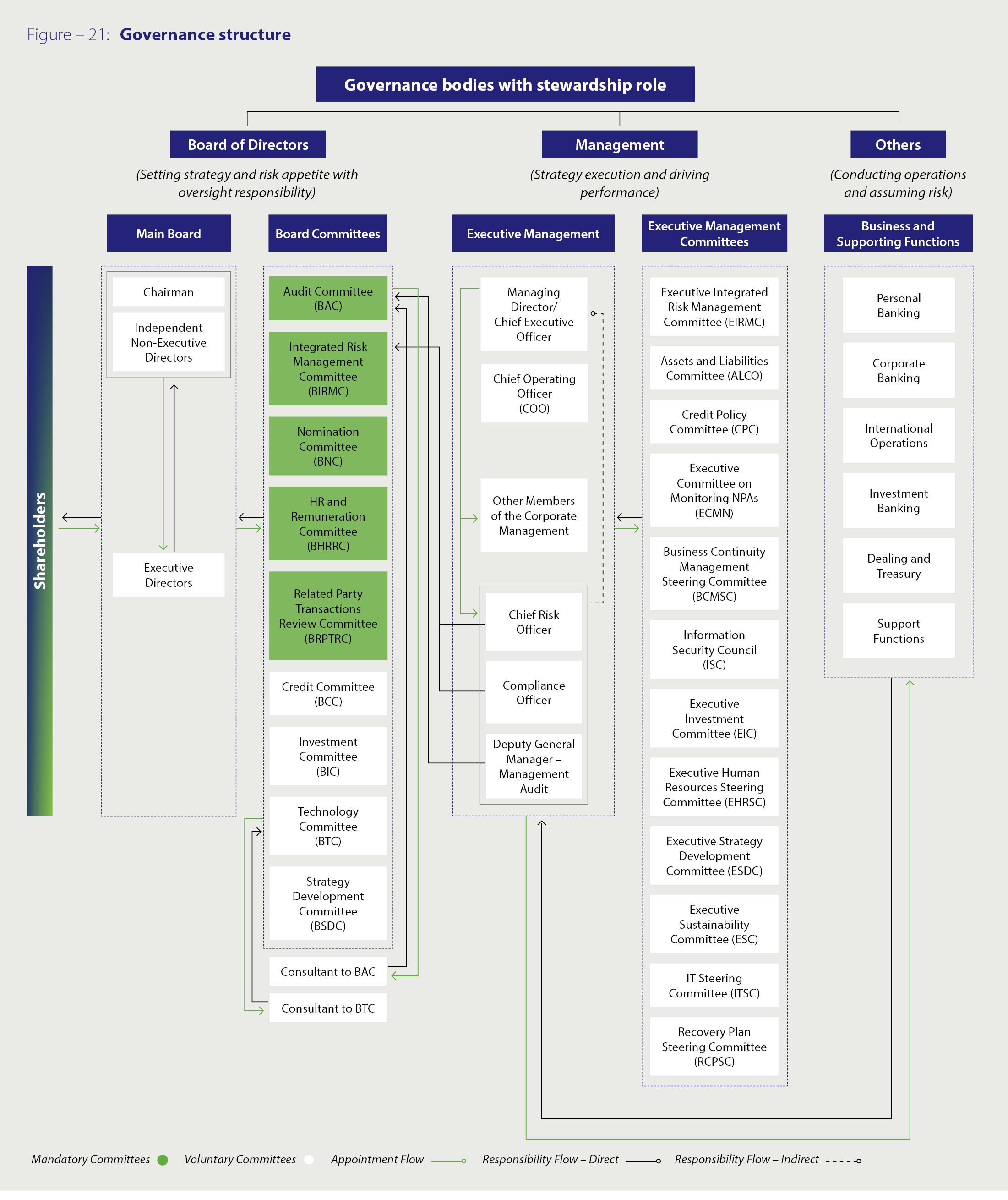

Governance structure

The Bank has a Board approved organisation chart, clearly depicting work responsibilities and reporting relationships (Refer Annex 7 for an abridged organisation chart ).

The foundation of the governance structure of the Bank is built on well-defined roles and responsibilities, greater accountability, and clear reporting lines of the Board, Board Committees, Management, and Management Committees. The Board and Board Committees assisted by consultants where necessary are responsible for setting the strategy, defining the risk appetite, and exercising oversight while Management and Management Committees are responsible for executing the strategy and driving performance. Responsibility and accountability for conducting operations and assuming risk under the purview of the Management lie with the strategic business units and support functions. The governance structure of the Bank is given in Figure 21.

Board of Directors (Principles A.1, A.1.5, A.4, and A.10)

The Board of Directors plays a pivotal role in demonstrating good corporate citizenship, ethical behaviour, transparency, and accountability whilst also warding off all forms of corporate malfeasance. The Board of Directors – the highest decision-making authority with responsibility for the sustainability of the Bank provides leadership by setting strategic direction, defining risk appetite, approving remuneration policies, and making appointments to the Board and the Corporate Management. Under the due diligence and oversight of the Board, Corporate Management is responsible for the execution of the strategy, day-to-day operations, and implementing an effective system of internal control. The Board and Corporate Management have a clear mutual understanding of their respective roles, delegated authority, and boundaries. Based on trust and respect, the Board and the Corporate Management work within a productive and harmonious relationship which is a pre-requisite for good corporate governance and organisational effectiveness. This has proved to be one of the key reasons for the many achievements of the Bank and its positioning as the benchmark private sector bank in the country. Furthermore, the Bank is one of the two higher tier Domestic Systemically Important Banks (D-SIBs) in Sri Lanka, currently having the Highest Loss Absorbency rate.

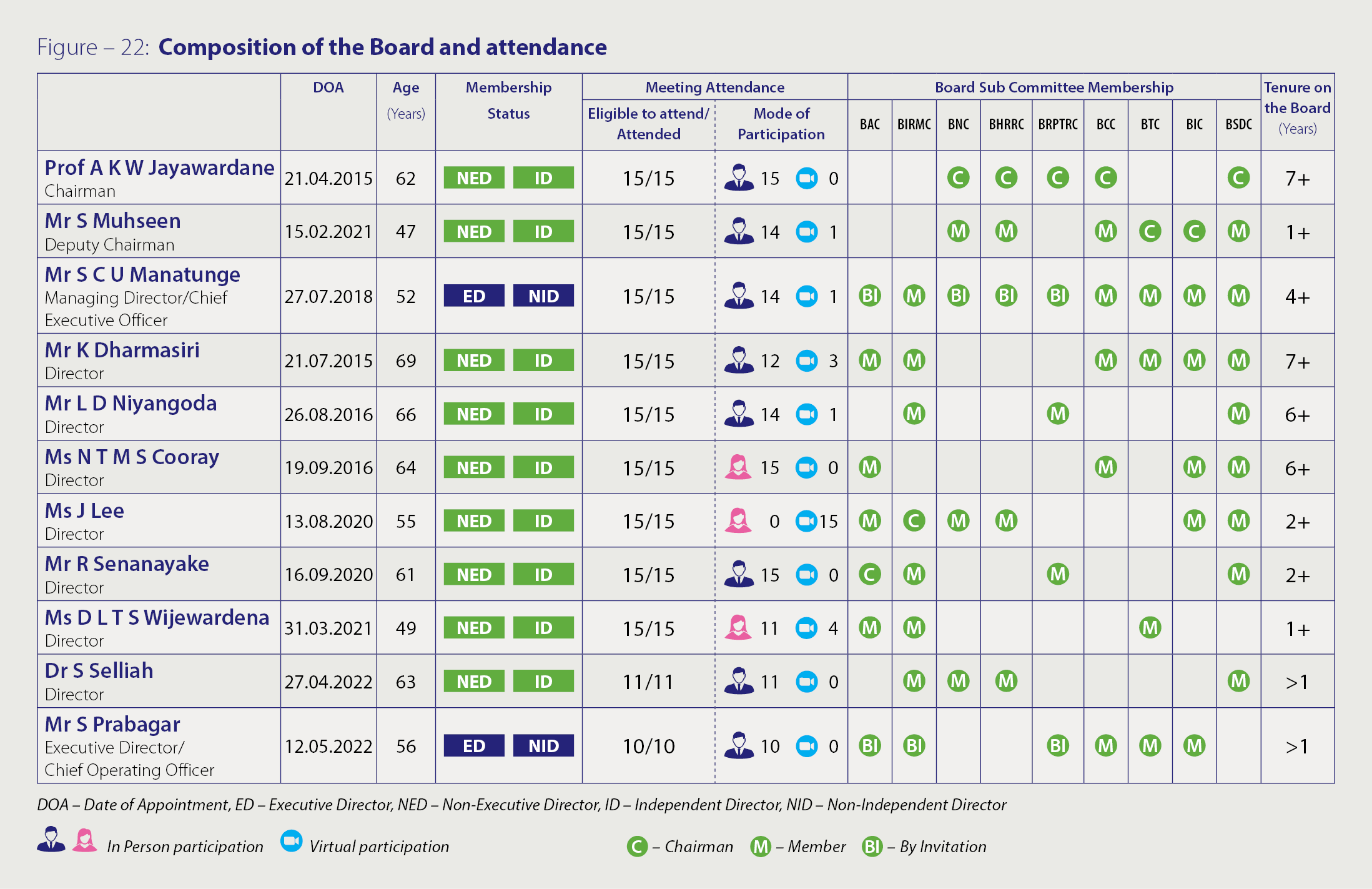

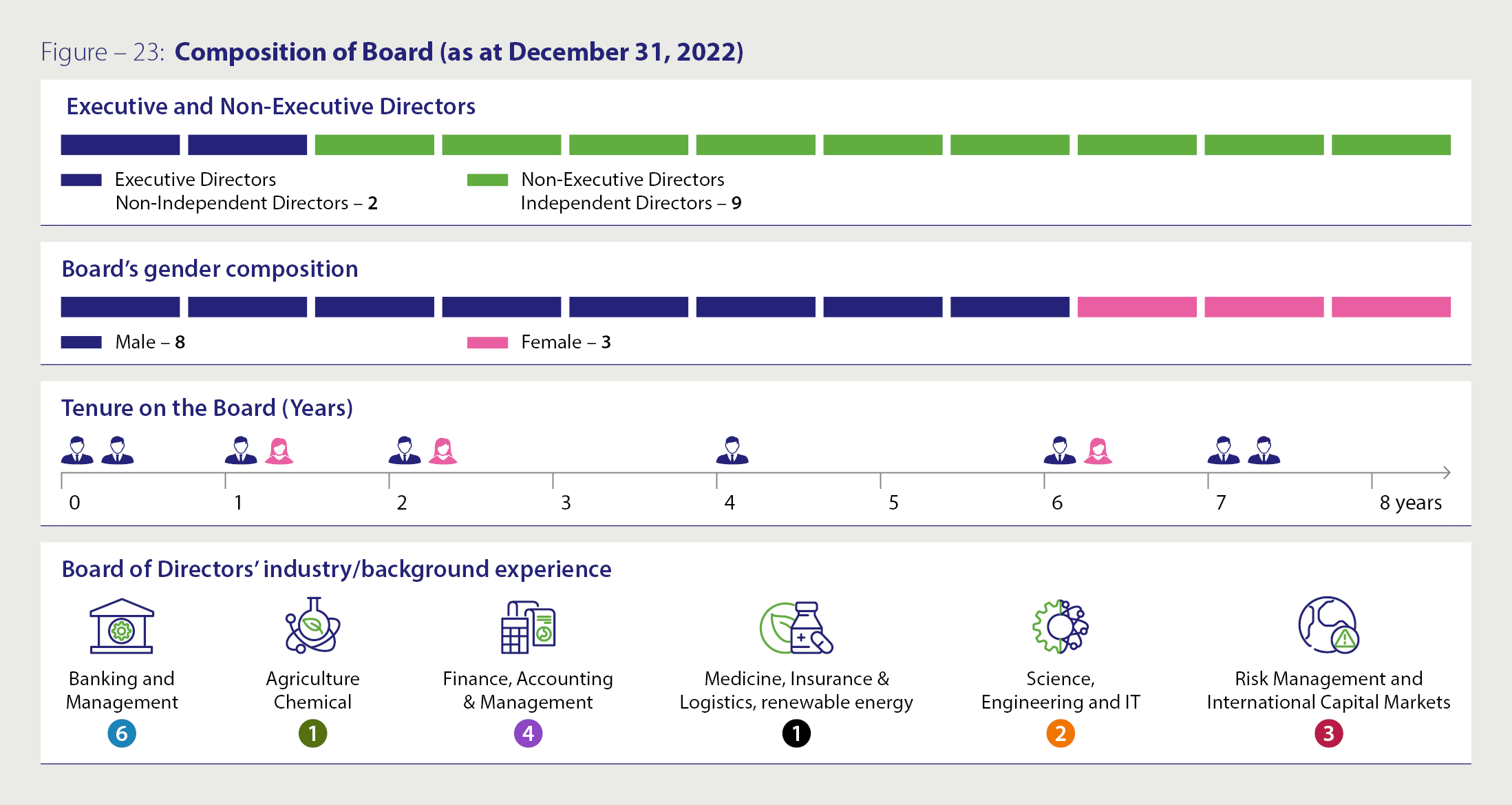

The Board comprised eleven Directors at end of 2022 (twelve as of the end of 2021). Each Director is an eminent professional in his or her respective field and holds the skills and expertise necessary to constructively challenge the Management and enrich deliberations on matters set before the Board. They understand and appreciate the dynamism and complexity of the operations of the Bank, its subsidiaries, and its associate, particularly in the wake of emerging global developments threatening to challenge conventional business models. Nine of the Directors (ten as of the end of 2021) are Independent Non-Executive Directors (INEDs), ensuring a higher degree of autonomy. Directors act in the best interest of the shareholders, avoiding any conflicts of interest.

Diversity and inclusion

Diversity and inclusion go hand in hand at the Bank, with the voices of a diverse range of people being inclusively heard in the working environment, all towards the overall progress of the Bank.

The Board of Directors mirrors this diversity and inclusion with expertise in accounting, banking and finance, economics, agriculture and chemical industry, engineering, information technology, risk management, manufacturing, healthcare, insurance, logistics, plantations, renewable power, and international capital markets. Having risen to the highest echelons of Government institutions or private sector organisations, they bring their independent judgement to bear on matters reserved for the Board. Bringing together banking, entrepreneurial, investor, and regulatory perspectives, the Board is able to explore matters from diverse points of view to facilitate long-term value creation. The Company Secretary assists the Board in discharging its responsibilities.

The diversity in the Board's composition has enabled it to bring a unique perspective to the Boardroom, enhancing dynamics and effectiveness while promoting a healthy and constructive exchange of views, leaving no room for groupthink.

The profiles of the Board members which include the qualifications, memberships in Board Committees, and both current and previous significant appointments as well as the profile of the Company Secretary are given in the section on Board of Directors and profiles.

Board process (Principles A.1.6, A.1.7, and A.6)

The Board agrees on a schedule of meetings at the beginning of each year and meets at least once a month. Additional meetings are also convened if required. With the assistance of the Company Secretary and in consultation with the Managing Director/ Chief Executive Officer, the Chairman is responsible for determining and preparing the agenda for the meetings. Board members also have the opportunity to propose items for inclusion in the agenda for discussion. The agenda, together with the accompanying Board papers, is circulated to the members of the Board by the Company Secretary, one week in advance of the dates fixed for the meetings. This provides the Board members with adequate time to study the contents, call for additional information if required, and be prepared for productive deliberations. The agenda and all Board Papers are circulated electronically to the Board members via the BoardPAC, ensuring absolute confidentiality of the information, providing instantaneous delivery, and of equal importance, cost saving on printing of papers, which is one of the many green initiatives of the Bank. This system helped the Bank to conduct Board and Board Committee meetings uninterrupted even during times when the physical presence was challenging. The Directors regularly attend the meetings, physically and/or virtually, and actively participate in deliberations. Urgent Board papers are submitted at short notice or tabled at the meetings on an exceptional basis. Board members typically spend, at a minimum, seven days a month on Board-related matters. In the best interest of the Bank, one-third of the Directors can call for a resolution to be presented to the Board, if required.

Minutes of deliberations and decisions made at the meetings are maintained in sufficient detail. If the need arises, members of Corporate Management are invited to make presentations to the Board on the performance of areas coming under their purview. Members of the Board are also allowed to seek independent professional advice, if necessary, at the Bank’s expense. The Bank has also obtained a Directors’ and Officers’ Liability Insurance Policy, affording them protection against any allegations in the conduct of their duties.

Conflicts of interest (Principle A.10)

The Bank has a meticulous system in place to avoid conflict of interest. At an individual level, members of the Board declare a situation of a conflicts of interest and withdraw from participating in deliberations on/exercising influence over matters where conflict or the appearance of conflict of interest arises. The actions are appropriately minuted for future reference. In addition, the affiliations and transactions of Directors are regularly reviewed to ensure that there are no conflicts or relationships that might impair Directors’ independence. The Board-approved Related Party Transactions Policy of the Bank sets out the procedure to be adopted in granting accommodations to the Directors, their close family members, and entities in which the Directors hold directorships, as permitted by the rules and regulations of the CBSL and within the terms and conditions such facilities are provided to other customers of the Bank. Such facilities, if any, are reviewed and recommended by the Board Credit Committee (BCC) and are submitted to the Board for approval. Once approved, details of such facilities are tabled at the next scheduled meetings of the Related Party Transactions Review Committee (BRPTRC) for information. The section on “Directors’ Interest in Contracts with the Bank" on discloses the details of transactions carried out in the ordinary course of business on an arm’s length basis with entities where the Bank’s Chairman or Directors serve as the Chairman or as a Director in another entity, while Note 62 to the Financial Statements includes information on Related Party Disclosures. At the point of joining and annually thereafter, the Directors declare their interests, and the necessary procedures in place to ensure that there are no conflicts of interest that will compromise the independence of members. A register of such declared interests is maintained by the Company Secretary and is available for inspection by shareholders or their authorised representatives as required by Section 119 (1) (d) of the Companies Act No. 07 of 2007 and amendments thereto.

Board meetings (Principle A.1.1)

In the year 2022, the Board held fifteen scheduled meetings (fifteen in 2021) of which one meeting (one meeting in 2021) was allocated exclusively to deliberations on Corporate Plan 2023 – 2027 and Budget 2023, with the members of the Corporate Management being present. Thirteen meetings (thirteen meetings in 2021) were devoted to matters including large and material transactions, review of performance, review and approval of a revised budget for 2022, review of policy frameworks, capital augmentation plan, recovery plan, reclassification of financial assets, recovery actions, strategy, review of investment strategies, and risk. Subsequent to the election/re-election of Directors at the Annual General Meeting (AGM) in place of those who retired by rotation, a further meeting was held to review and revise the composition of the Board Committees.

Figure 22 provides details of attendance at Board meetings including membership status, mode of attendance, positions held by the Board members in Board committees, and the tenure on the Board.

Such meetings are seen to provide an effective forum for discharging the oversight responsibility of the Board. Although the outbreak of the COVID-19 pandemic resulted in the physical format of these meetings needing to change, creating a new challenge to holding such meetings, the Bank successfully handled the transition to virtual platforms. All meetings of the Board and Board Committees were conducted in accordance with guidelines issued by the health authorities, with limited physical attendance with some Directors connected via virtual platforms. As such, the Bank showcased its ability to adapt to the new normal during the pandemic, thereby demonstrating its commitment to good corporate governance.

The Board continued to play an active role in strategy formulation, providing directions to the Corporate Management for the preparation of the Bank’s five-year strategic plan spanning 2023-2027. This plan was then reviewed and approved at a meeting specifically convened for this purpose, in December 2022. The meeting saw members of the Corporate Management present plans on areas coming under their purview, and extensive deliberations were made on said presentations, with the Board exploring and evaluating alternative strategies prior to the approval and allocation of resources for execution of the same. The Board continued to give prominence to liquidity and capital management in the wake of the sharp rise in market interest rates, the deficit in market liquidity, higher credit losses necessitated for foreign currency-denominated Government securities consequent to the downgrade of the country’s sovereign rating, and the Government’s announcement to restructure foreign currency debt, deteriorating credit quality, and increasing tax burden, all in a bid to support growth and ensure sustainable value creation. One of the regular items on the agenda at the monthly Board meetings is to review performance against the strategic plans, allocating sufficient attention and time to review the progress and to identify areas of concern requiring further attention by the Board. In addition, the Board heightened its attention on credit quality, closely monitored exposures to risk-elevated industries, reviewed the appropriateness of the impairment methodology, monitored movements in staging of exposures, and sought to resolve distressed credit facilities. Furthermore, through periodic presentations made by the respective Chief Executive Officers and/or Managing Directors, the Board also reviewed the performance and future plans of the subsidiaries of the Bank. Due to the new directions issued by the CBSL – Direction No. 13 of 2021 on Classification, Recognition, and Measurement of Credit Facilities and Direction No. 14 of 2021 on Classification, Recognition, and Measurement of Financial Assets other than Credit Facilities in Licensed Banks - which became effective from January 01, 2022, the Board also reviewed the changes these Directions would require to be made to existing policies, processes and newly introduced policies of the Bank.

Board Committees (Principles A.7.1, D.3, and D.4)

Board Committees are appointed both in terms of compulsory requirements and voluntarily. Out of the Nine Board Committees that have been appointed with delegated authority to strengthen governance and to deal with/decide on certain subject-specific and specialised matters, five are mandatory whilst four are voluntary. Four out of five mandatory Committees have been formed as required by the Direction, while the BRPTRC has been formed as required by the provisions of the SEC of Sri Lanka. The four voluntary Board Committees have been established considering the business, operational, information technology, and strategy development needs of the Bank as permitted by the Bank’s Articles of Association. Constituted with Board-approved Terms of Reference, these Committees hold regular meetings – once a quarter at a minimum. The Board Committees have sought guidance and advice from external consultants on several occasions. Furthermore, each of the Directors served in a minimum of three Committees during the year. The Board, however, retains responsibility for all Committee decisions, thereby ensuring the continuance of good corporate governance.

Minutes capturing the proceedings of the Board Committee meetings were regularly tabled at the Board meetings for information/approval of the members, and any concerns identified in relation to specialised areas were also referred to them for oversight. The minutes for these meetings, carefully ascertain and record the views and deliberations of the Directors on issues under consideration.

The composition, areas of oversight responsibility under respective mandates, key activities in 2022, and attendance of members at the Board Committee meetings are given in the respective Board Committee reports.

Executive Management Committee

The Executive Management Committee (EMC) comprises all members of the Corporate Management including the Managing Director/Chief Executive Officer (MD/CEO) and the Chief Operating Officer (COO), who are also the two Executive Directors (EDs) of the Bank. The primary responsibility of the EMC is to implement strategy - as approved by the Board under the leadership of the MD/CEO – and deliver on the performance objectives while ensuring that the risks undertaken by the Bank are within the risk profile approved by the Board. The EMC has several responsibilities such as laying down policies, making operational decisions, monitoring financial performance against budgets, reviewing the achievement of strategic goals set for business divisions, allocating capital, monitoring the progress of implementing the Digital Road Map, managing risk, deliberating on human resource development including health and safety, fortifying the compliance function, implementing the Sustainability Framework and solving operational and customer issues. Beyond the above functions, the EMC also reviews and deliberates information prior to Board review, thereby ensuring that the Board is provided with all material information in a timely and detailed manner, thus aiding the Board to effectively fulfil their oversight responsibilities as Directors. In addition, the EMC meetings provide all members with the opportunity to gain a 360o view of the Group’s operations.

Members of the Corporate Management including the MD/CEO review the operations of the subsidiaries and the associate of the Bank to safeguard the Bank’s interest and ensure a reasonable return thereon.

The names, designations, qualifications, and experience of the members of the EMC are given under Corporate Management and Profiles, while the names of Senior Management related to the Bank’s operations in Sri Lanka, Bangladesh, the Maldives, Myanmar, and the subsidiaries in Sri Lanka are given in the section on Senior Management.

Management Committees

In addition to the Board, the Board Committees, and the EMC, several other Management Committees have been established for good governance along subject-specific lines to facilitate decision-making and executing Board-approved strategies. These Management Committees operate under delegated authority from the MD/CEO.

Based on approved Terms of Reference, the Management Committees operate under a structure and a process similar to that of the Board Committees. Detailed minutes are recorded by the Secretary of the respective Committee, which are then submitted to the relevant Board Committees after approval by the MD/CEO. These Committees undertake extensive deliberations, cooperate across departments, and debate on matters considered critical for the Bank’s operations as described in the Figure 24 below.

Figure-24: Executive Management Committees

Executive Integrated Risk Management Committee (EIRMC)

Purpose and tasks

Monitors and reviews all risk exposures and risk-related policies and procedures affecting credit, market and operational areas in line with the directives from the BIRMC.

Composition

MD/CEO, COO and key members of Integrated Risk Management, Personal Banking, Corporate Banking, Treasury, Internal Audit, Compliance, Finance and Information Security Divisions.

Meeting frequency: Monthly

Assets and Liabilities Committee (ALCO)

Purpose and tasks

Optimises the Bank’s economic goals whilst maintaining liquidity and market risk within the Bank’s predetermined risk appetite.

Composition

MD/CEO, COO and key members of Treasury, Corporate Banking, Personal Banking, Integrated Risk Management, Marketing and Finance Divisions.

Meeting frequency: Fortnightly

Credit Policy Committee (CPC)

Purpose and tasks

Reviews and approves credit policies and procedures pertaining to the effective management of all credit portfolios within the lending strategy of the Bank.

Composition

MD/CEO, COO and key members of Corporate Banking, Personal Banking, Integrated Risk Management, Internal Audit, Marketing and Credit Supervision & Recoveries Divisions.

Meeting frequency: Quarterly

Executive Committee on Monitoring NPAs (ECMN)

Purpose and tasks

Reviews and monitors the Bank’s Non-Performing Advances (NPAs) above a predetermined threshold to initiate timely corrective actions to prevent/reduce credit losses to the Bank.

Composition

MD/CEO, COO and key members of the Corporate Banking, Personal Banking, Credit Supervision & Recoveries, and Integrated Risk Management Divisions.

Meeting frequency: Monthly

Business Continuity Management Steering Committee (BCMSC)

Purpose and tasks

Directs, guides, and oversees the activities of the Business Continuity Plan of the Bank in accordance with the Bank’s strategy.

Composition

COO and key members of Human Resources Management, Personal Banking, Corporate Banking, IT, Services, Operations, Integrated Risk Management and Internal Audit.

Meeting frequency: Quarterly

Information Security Council (ISC)

Purpose and tasks

Focuses continuously on meeting the information security objectives and requirements of the Bank in line with emerging technology and Bank's Strategy.

Composition

MD/CEO, COO and key members of Human Resources Management, Services, Operations, IT and Information Security, Internal Audit, Integrated Risk Management, Compliance and Legal Divisions.

Meeting frequency: Monthly

Executive Investment Committee (EIC)

Purpose and tasks

Oversees investment activities by providing guidance to the management on significant investment decisions and reviews performance.

Composition

MD/CEO, COO and key members of Corporate and Personal Banking, Investment Banking, Treasury, Finance and Planning Divisions.

Meeting frequency: Quarterly

Executive Human Resources Steering Committee (EHRSC)

Purpose and tasks

Setting guidelines and policies on any matter that may affect the Human Resource Management of the Bank and make recommendations on policy matters to the BHRRC and/or address any issues that may need to be reviewed at Board level.

Composition

MD/CEO, COO and key members of Human Resources Management, Personal Banking, Corporate Banking, Marketing, Finance and Treasury, Integrated Risk Management, Internal Audit and IT Divisions.

Meeting frequency: Quarterly

Executive Strategy Development Committee (ESDC)

Purpose and tasks

Based on overall insights provided by the BSDC, formulates strategies geared for the sustainable development of the Bank. Monitors the implementation of the approved strategic plan and the progress made against strategic milestones and goals.

Composition

MD/CEO, COO and key members of Human Resources Management, Marketing, Personal Banking, Corporate Banking, Treasury, Finance and Planning, Integrated Risk Management and IT Divisions.

Meeting frequency: Quarterly

Executive Sustainability Committee (ESC)

Purpose and tasks

To help advance the Sustainability agenda and performance of the Bank, directing Banks’ activities to be in line with the regulatory requirements of the CBSL on Sustainable Finance Roadmap and Principles of the Sri Lanka Banks’ Association sustainable banking voluntary initiatives, while assisting the Board to oversee and approve the implementation of sustainable policies, objectives and targets.

Composition

MD/CEO, COO, and key members of Integrated Risk Management, Services, Corporate Banking, Personal Banking, Investment Banking, Human Resource Management, and Retail Banking & Marketing.

Meeting frequency: Bi-annually

IT Steering Committee (ITSC)

Purpose and tasks

Assist the Management Committee and the Board of Directors to fulfil its overseeing responsibilities with respect to the overall role of technology, in executing the business strategy of the Bank including but not limited to, major technology investment, technology strategy, operational performance and technology trends that may affect future banking.

Composition

COO, and key members of Corporate Banking, Personal Banking, Treasury, Human Resource Management, Integrated Risk Management, Retail Banking & Marketing, Management Audit, IT, Services and Operations.

Meeting frequency: Monthly

Recovery Plan Steering Committee (RCPSC)

Purpose and tasks

Exercises the powers and authority entrusted by the Board/Corporate Management with respect to formulating, maintaining, regularly reviewing, executing, coordinating, activating the Bank’s recovery plan to deal with shocks to capital, liquidity and all other aspects that may arise from institution-specific market wide stresses.

Composition

COO, and key members of planning, Integrated Risk Management, Finance, Corporate Banking, Personal Banking, Treasury, Human Resource Management, Marketing, Management Audit, Compliance, IT, and Operations.

Meeting frequency: Quarterly

Roles, responsibilities, and powers of the Board (Principles A.1.2 and A.1.3)

The role of the Board of Directors and their responsibilities are set out in the Board Charter, which includes a schedule of powers reserved for the Board as detailed below:

Role of the Board

- To represent and serve the interests of shareholders by overseeing and appraising the Bank’s strategies, policies, and performance

- To provide leadership and guidance to Management for the execution of strategies

- To optimise performance and build sustainable value for shareholders in accordance with the regulatory framework and internal policies

- To establish an appropriate governance framework

- To ensure regulators are apprised of the Bank’s performance and any major developments

- To review the performance of the business against the goals and objectives at regular intervals

Key responsibilities

- Selecting, appointing, and evaluating the performance of the MD/CEO

- Setting strategic direction and monitoring its effective implementation

- Establishing systems of risk management, internal control, and compliance

- Ensuring the integrity of the financial reporting process

- Developing a suitable corporate governance structure, policies, and framework

- Strengthening the safety and soundness of the Bank

- Reviewing the performance of the Bank and the Group companies

- Appointing members to the Board of Directors to fill casual vacancies

- Appointing members of the Corporate Management of the Bank

- Appointing and overseeing the External Auditors’ Responsibilities

- Approving Interim and Annual Financial Statements for publication

Powers reserved for the Board

- Approving major capital expenditure, acquisitions, and divestitures, and monitoring capital management

- Appointing the Board Secretary in accordance with Section 43 of the Banking Act No. 30 of 1988

- Seeking professional advice in appropriate circumstances at the Bank’s expense

- Reviewing, amending, and approving governance structures and policies

Board’s role in risk management (Principle D.2)

Risk management is key to the long-term sustainability of the Bank. The Board, as the highest decision-making authority in the Bank, is responsible for implementing an effective risk management mechanism across the Group. With the support of the BIRMC, the Board has devised an effective risk management framework that sets the risk appetite and tolerance limits, facilitating monitoring of the risk profile on a regular basis through risk reports submitted to the Board. Risk management has continued to be one of the key and regular items on the agenda of Board and relevant Board Committees meetings. Clarifications were sought from the respective members of the Management for any deviations from the agreed risk profile and necessary guidance was given for taking mitigatory action. Further, risks related to the business strategies were carefully reviewed at a special Board meeting held to review the Budget for the year 2023 and deliberate on the strategic plan 2023-2027 (Refer Risk Governance and Management for further details).

Figure – 25: Board Highlights 2022

| 1 |

Approval/recommendation of a First and Final dividend for the year ended December 31, 2021 of Rs. 7.50 per share, constituting a total sum of Rs. 8,956,659,742.50, distributed by way of cash of Rs.4.50 per share and by the allotment and issue of new shares of Rs. 3.00 per share. |

| 2 |

Conducted the Annual General Meeting virtually by using a digital platform in line with the guidelines issued by the regulators. |

| 3 |

Approval/recommendation to issue and allot up to 100,000,000 fully paid, Basel III Compliant – Tier II, Subordinated, Redeemable Debentures at a par value of Rs. 100/- each. |

| 4 |

Conducted an Extraordinary General Meeting to obtain approval for the debenture issue 2022 in the form of a physical meeting. |

| 5 |

In view of the retirement of the former Chairman, the existing Deputy Chairman at that time was appointed as the Chairman of the Bank in March 2022, and a new Deputy Chairman was appointed from and among the existing members of the Board. |

| 6 |

In view of the retirement of the former Managing Director, the existing Chief Operating Officer at that time was appointed the Managing Director of the Bank in May 2022, and a new Director was appointed to the Board as a non-independent/Executive Director/Chief Operating Officer. |

| 7 |

A new independent/non-executive Director was appointed to further strengthen the Board. |

| 8 |

Reviewed the Composition of Board and Board Committees, respective Committee Charters and Terms of Reference. |

| 9 |

The Board of Directors participated in a high-level web conference on Key Aspects of Anti Money Laundering/Combating Financing of Terrorism compliance for the Board of Directors and Key Management Personnel conducted by the Central Bank of Sri Lanka. |

| 10 |

Conducted a training programme on Information Security Awareness for the Board of Directors by an external resource person. |

| 11 ; |

Reviewed all major policy documents. |

| 12 |

Annual strategy meeting with Corporate Management Team. |

| 13 |

Based on recommendations made by the Board Nomination Committee, the Board approved the appointment of a Chief Information Officer. |

| 14 |

Based on recommendations made by the Board Nomination Committee, the Board approved the appointment of an Assistant General Manager, the re-designation of a Deputy General Manager, and the promotion of three Assistant General Managers to the Deputy General Manager Grade. |

| 15 |

Approved a Group Conduct Risk Management Policy Framework to ensure fair treatment to customers, protection of financial markets, and promotion of competition. |

Segregation of roles of Chairman and Chief Executive Officer (Principles A.2 and A.3)

The positions of the Chairman and the Chief Executive Officer are separated, to facilitate the balance of power and authority, and to adhere to the best practice in Corporate Governance. The Chairman is a Non-Executive Independent Director while the Chief Executive Officer is an Executive Director appointed by the Board. Their respective roles are clearly set out in an approved Board paper and the Board Charter of the Bank.

Accordingly, as set out in the said Board paper and the Board Charter, a clear and effective separation of accountability and responsibility has made the role of the Chairman distinctive. By providing leadership to the Board, preserving order, and facilitating the effective discharge of its duties, the Chairman promotes good corporate governance and the highest standards of integrity, and probity throughout the Group. He ensures that the Board receives all information necessary for making informed decisions in discharging its responsibilities. The Chairman also ensures that a balance of power is maintained between executive and non-executive Directors and the Board is in full control of the Bank’s affairs and is alert to its obligations to all stakeholders. Furthermore, he also ensures the effective participation of all Directors in Board deliberations and maintains open lines of communication with members of the Corporate Management, providing an effective platform for deliberating strategic and operational matters.

On the other hand, the role of the Chief Executive Officer, as set out in the Board Charter, is to conduct the management functions as directed by the Board. The corporate objectives and the boundaries of his authority as Chief Executive Officer are set by the Board, while his duties and responsibilities are jointly developed.

The Chief Executive Officer leads the Management team in the day-to-day operations and ensures the implementation of strategies, plans, and budgets approved by the Board. The Chief Executive Officer conducts the affairs of the Group, upholding good corporate governance, and the highest standards of integrity and probity as established by the Board.

While they have separate functions, the Chairman and the Chief Executive Officer meet regularly to set the Board agenda, deliberate on current and future developments, and discuss any material issues impacting the Bank, thereby working together toward the Bank’s overall progress.

Role of Independent Non-Executive Directors

The Bank has a strong element of independence on the Board, with nine out of the eleven Directors as of December 31, 2022 being INEDs. The only connection of the independent Directors with the Bank and with other Companies in the Group is their directorships, thereby ensuring that their judgement is unlikely to be influenced by external considerations. The presence of INEDs is expected to complement the skills and experience of the other Board members through the INEDs conveying an objective and independent view on matters, using their expertise to challenge the Board and the Management constructively, and by assisting in guiding the strategy.

Role of the Company Secretary (Principle A.1.4)

The Company Secretary plays a vital role in facilitating good Corporate Governance. His responsibilities encompass activities relating to Board meetings, general meetings, Articles of Association, reports, accounts and documentation, Corporate Governance, and Stock Exchange requirements. Primary responsibilities include:

- Assisting the Chairman in conducting the Board Meetings, AGMs, and EGMs in accordance with the Articles of Association, the Board Charter, and relevant legislation

- Maintaining minutes of meetings and statutory registers, and filing statutory returns on time

- Monitoring all Board Committees to ensure they are properly constituted and have clearly defined Terms of Reference

- Facilitating best practices of Corporate Governance including assisting the Directors with their duties and responsibilities

- Facilitating access to legal and independent professional advice in consultation with the Board, where necessary

- Ensuring the Bank complies with its Articles of Association incorporating the required amendments, following proper procedure

- Coordinating the publication and distribution of the Bank’s Annual Reports and Accounts and interim financial statements, and preparing the Directors’ Report

- Monitoring and ensuring compliance with Listing Rules including required disclosure on related parties and related party transactions, and maintaining cordial relationships with the CSE, share and debenture holders

- Communicating promptly with the regulators

The appointment and removal of the Company Secretary are done by the Board.

Appointments and retirements/resignations of Directors (Principle A.7)

The appointment of new Directors is based on an annual assessment of the combined knowledge, experience, and diversity of the Board, with new Directors chosen on their ability to bring added perspective and ensure the continued effectiveness of the Bank’s strategic plans. Accordingly, the nomination of candidates for appointment as Directors takes place under a formal and transparent procedure formulated by the BNC. The resumés of potential candidates are carefully evaluated by the BNC prior to them being recommended to the Board for their consideration as NEDs. Such nominations may also include an interview with the candidate.

A similar process is followed when appointing EDs, with the exception of when candidates are selected from the Corporate Management of the Bank.

As required by the Listing Rules, appointments of new Directors to the Board are promptly communicated to the CSE through announcements, subsequent to obtaining approval from the CBSL for their fitness and propriety. The announcements typically include a brief resumé of new Directors, relevant expertise, key appointments, shareholdings, and status of independence. In addition, all the staff members of the Bank are informed of any new appointments to/resignations and retirements from the Board as well as the appointment of Directors to the positions of the Chairman and the Deputy Chairman via internal circulars.

The retirements or resignations of Directors are promptly communicated to the CSE as required by the Listing Rules.

During the year under review, there were two new additions and three retirements including the former Chairman and the former Managing Director from the Board of Directors, the details of which are given in Figure 22 titled Composition of the Board and Attendance.

Re-election/election of Directors (Principle A.8)

The Articles of Association of the Bank state that the two longest-serving NEDs must offer themselves for re-election at each AGM in rotation, with the period of service being considered from the last date of re-election or appointment. If two or more Directors qualify for re-election in a particular year, the Directors may decide amongst themselves, either by considering the affidavits and declarations submitted by them and all other relevant issues or by drawing lots to determine which Directors will offer themselves for re-election. Accordingly, Ms N T M S Cooray and Ms J Lee, the two longest-serving Directors since their last re-election will be seeking re-election at the forthcoming AGM to be held on March 30, 2023. In addition to the above clauses, if a Director has been appointed as a result of a casual vacancy that has arisen since the previous AGM, that Director will also offer himself/herself for election at the immediately succeeding AGM. Accordingly, Dr S Selliah, Ms S Prabagar and Mr D N L Fernando who were appointed to the Board in April 2022, May 2022 and in February 2023 respectively, to fill casual vacancies will offer themselves for re-election at the forthcoming AGM.

Induction and training of Directors (Principle A.1.8)

On appointment, Directors are provided with an induction pack that outlines the main areas that require familiarisation. The pack includes the Articles of Association, the Banking Act Directions, the Corporate Directors’ Handbook published by the Sri Lanka Institute of Directors, the Code of Best Practice on Corporate Governance 2017 issued by CA Sri Lanka, the Bank’s organisational structure, copies of the Board Charter and the Board Related Party Transactions Policy, and the most recent Annual Report of the Bank. They are also given access to the electronic support system which has archived minutes of meetings held over the past ten years. All Directors are encouraged to obtain membership in the Sri Lanka Institute of Directors which conducts useful programmes to support Directors. Furthermore, it is mandatory for Directors to attend Director Forums organised by the CBSL. As additional support, members of the Corporate Management and external experts make regular presentations on the business environment in relation to the operations of the Bank, which enables newly appointed Directors to familiarise themselves with the banking operations.

Remuneration and Benefits Policy

The Remuneration and Benefits Policy seeks to provide a distinctive value proposition to current and prospective employees to attract and retain employees with the skills and values that are in line with the business needs of the Bank. The Policy also provides a framework for the Bank to design, administer, and evaluate effective reward programmes, thereby inspiring and motivating desired behaviours, and enabling proper alignment of remuneration with the long-term success of the Bank.

Directors’ and Executive remuneration (Principles A.10, B.1 and B.3)

The Bank has a number of processes in place to ensure that no individual Director is involved in determining his or her remuneration but is instead part of a larger deciding process that makes final decisions. Primarily, the BHRRC- which consists entirely of NEDs who also meet the criteria for independence as set out in the relevant regulations on corporate governance- is responsible for making recommendations to the Board regarding the remuneration of the Directors and executives. The BHRRC in consultation with the MD/CEO and after obtaining professional advice, where necessary, makes such recommendations.

Remuneration for Directors and executives is further set out with reference to the Remuneration and Benefit Policy. The remuneration for NEDs is set by the Board as a whole. In order to provide fair judgements when discharging their duties on remuneration, the Board and the BHRRC engage the services of HR professionals on a regular basis as well.

Details of the Remuneration paid to Directors are given in Note 21 to the Financial Statements.

The level and make-up of remuneration (Principle B.2)

It is the responsibility of the BHRRC to ensure that the remuneration of both EDs and NEDs is sufficient to attract eminent professionals to the Board and retain them to drive the performance of the Bank. The Bank has remuneration policies that are attractive, motivating, and capable of retaining high-performing, qualified, and experienced employees.

With the assistance of professionals, the BHRRC structures the remuneration packages and benchmarks them with the market on a regular basis to ensure that total remuneration levels remain competitive to attract and retain key talent whilst balancing the interests of the shareholders. The total remuneration of EDs and other members of the Corporate Management includes three components – guaranteed remuneration (the fixed component), annual performance bonus (a variable component), and the ESOP (a variable component). Special emphasis is paid to making the basis of granting ESOPs and their features transparent, prior to seeking approval from the shareholders.

Guaranteed remuneration comprises the monthly salary and allowances determined with due reference to the qualifications, experience, levels of competencies, skills, roles, and responsibilities of each employee. These are reviewed annually and adjusted for factors such as promotions, performance, and inflation. The annual performance bonus is based on the degree of achievement on a multi-layered performance criteria matrix which is clearly communicated to the relevant category of employees at the beginning of each year. The Bank maintains a regular dialogue and consults when necessary its two employee associations – the Association of Commercial Bank Executives and the Ceylon Bank Employees’ Union (CBEU). In early January 2021, the Bank signed the Collective Agreement with the CBEU covering a three-year period from 2021-2023, after extensive deliberations.

With a view to motivate employees to commit to long-term value creation, improve overall performance, and increase staff retention while raising equity funding, the Bank has structured many Employee Share Option Plans (ESOPs) since 1997. This entitles the eligible employees to buy a fixed number of shares at a price to be determined based on the pre-agreed formula over the vesting period. The Bank has duly obtained the approval of shareholders for all these ESOPs at Extraordinary General Meetings. The EDs, being employees of the Bank, are also eligible for these ESOPs.

Details of the ESOPs and the eligibility criteria are given in Note 52 to the Financial Statements on “Share-based Payment”.

While employment contracts do not contain any commitments for compensation or early terminations, there were no instances of early termination during the year that required compensation.

Board and Board Committee evaluations (Principle A.9)

As set out in the Direction, the Code, and the other applicable regulations, the Board and the Board Committees annually appraise their own performance to ensure that they are discharging their responsibilities satisfactorily in accordance with the Board Charter. This process requires each Director to fill out a Board Performance Evaluation Form incorporating all criteria specified in the Board Performance Evaluation Checklist of the Code. The responses are then collated by the Company Secretary and submitted to the BNC for consideration. These are subsequently discussed at a Board meeting. Board evaluations for 2021 and 2022 were taken up at the Board Meetings held in February 2022 and February 2023 respectively.

Appraisal of the Chief Executive Officer (Principle A.11)

With the assistance of the BHRRC, the Board assesses the performance of the Chief Executive Officer annually. This assessment is based on criteria agreed upon at the beginning of each year and consists of short, medium, and long-term objectives with financial and non-financial targets whilst also considering the changes in the operating environment. The Chairman discusses the evaluation with the Chief Executive Officer and provides him with formal feedback. The Chief Executive Officer’s responses to the appraisal are given due consideration prior to it being approved. This exercise is finalised within three months from the financial year end.

Shareholder engagement and voting (Principles C.1, C.2, E, and F)

The Bank actively engages with shareholders and potential investors as an aspect of good corporate governance and has established a structured process to facilitate the same. The Board-approved Shareholder Communication Policy is in place to ensure effective and timely communication of material matters to shareholders. The Bank maintains several communication channels with the shareholders which include the annual report, AGMs and EGMs, interim financial statements, announcements to the CSE, press releases, the Bank’s website, shareholder surveys on a need basis, and the investor feedback form on the Annual Report (Refer Table 3 on “How we connect with our stakeholders” for more details in this regard).

During the year, shareholders were notified - either through announcements made to the CSE or via media – about the quarterly results, dividend declaration for 2021, annual financial statements for 2021, interim financial statements for 2022, disclosure on Fitch Ratings Preview, appointments and retirements of Directors, the listing of shares issued as a part of the final dividend for 2021 as well as new shares listed consequent to the exercising of options under employee share option schemes, date of the Annual General Meeting 2023, dealings in shares of the Bank by Directors and related entities, Basel III compliant convertible debenture issue, and the extraordinary general meeting for the Basel III compliant convertible debenture issue. The Bank’s website was updated with new value-added features during the year and has a dedicated page for investors, ‘Investor Relations’ for investors which include interim financial statements and annual reports. The Bank’s annual report is offered in both PDF and interactive formats, providing readers with a choice for viewing. The interactive report also features a tab for investor feedback. The Board is fully committed to treating all shareholders equitably while recognising, protecting, and facilitating their rights through open communication. The Bank arranged to publish the interim and annual financial statements in the newspapers in all three mediums within statutory deadlines as per the Directions issued by the CBSL, and also submitted interim and annual financial statements to the CSE within the stipulated timeframes in terms of the Listing Rule No. 7.4 of the CSE. In addition, the Bank issues commentaries on the interim financial statements in the form of press releases to the media.

The Bank always encourages shareholders to participate in the AGMs and the EGMs and exercise their votes. To this end, the Bank circulates clear instructions on procedures governing voting along with every notice of AGMs/EGMs. Shareholders play a key role in the re-election of Directors and the External Auditor, and vote on all matters for which notice is given including the adoption of the annual report and accounts. Although the Bank could not conduct the AGM with the physical presence of its shareholders due to the outbreak of COVID-19 (as per the Notice of Meeting published in the Annual Report 2021), after giving due notice and publicity, it successfully conducted the Fifty-Third AGM as a virtual meeting. The AGM was conducted fully adhering to the guidelines issued by the Government health authorities and regulators while ensuring maximum shareholder participation, providing every opportunity for shareholders to clarify matters of interest to them. A total of 46 Voting and 1 Non-Voting shareholder participated in the Fifty-Third AGM held virtually on March 30, 2022, while further 137 Voting shareholders and 8 Non-Voting shareholders exercised their right to vote through proxy. The 8 Non-Voting shareholders exercised their right to vote through proxy strictly in relation to matters designated for their vote.

Shareholder approval was received at an EGM held on October 31, 2022 conducted with the physical attendance of shareholders for issuing Basel III compliant convertible debentures for augmenting Tier II capital and to support future lending growth of the Bank, raising Rs. 10.000 Bn. in Tier II capital consequently.

A tabulation of the details of shareholder attendance at AGMs during the past five years is given below:

Table – 47: Attendance at AGMs – 2018 to 2022

|

Voting shareholders

(including proxies) |

Non-voting shareholders

(including proxies) |

| Year of the AGM |

Number of

attendees |

Shareholding |

% of total

shareholding |

Number of

Attendees |

Shareholding |

% of total

shareholding |

| 2022 |

183 |

795,203,283 |

72.33 |

9 |

4,197,212 |

6.17 |

| 2021 |

169 |

795,052,531 |

72.32 |

19 |

4,326,942 |

6.36 |

| 2020 |

119 |

672,118,061 |

69.92 |

19 |

3,132,256 |

4.72 |

| 2019 |

346 |

703,703,954 |

73.21 |

145 |

12,048,304 |

18.18 |

| 2018 |

317 |

713,801,082 |

75.52 |

119 |

14,344,030 |

22.06 |

Whistleblowing

The Bank has adopted a Whistleblowers’ Charter to deter, detect, and address any genuine concerns of malpractices and unethical behaviour, with the Compliance Officer being appointed to manage the Bank’s whistleblowing processes.

In addition, measures have been put in place to protect whistleblowers who act in good faith in the interest of the Bank. The Bank undertakes to maintain the utmost confidentiality of the staff who raise concerns or make serious specific allegations of malpractice or unethical behaviour. In this way, the Bank aims to promote a healthy workplace that practices good governance from the lowest to the highest tiers.

Anti-Bribery and Anti-Corruption

The Bank reviewed and updated the Board-approved Anti-Bribery and Anti-Corruption Policy during the year, which sets out principles for countering bribery and corruption in the Bank. The principles also set out the management of bribery and corruption risk by requiring the Bank, Bank personnel, and defined third parties to commit to countering bribery and corruption in all forms in relation to transactions routed through or involving the Bank.

The Bank has zero tolerance for any form of bribery and corruption and will treat potential instances of bribery or corrupt behaviour as a threat to its integrity and reputation as a business. The Bank developed the Policy in accordance with these commitments as well as in adherence to the applicable laws and regulations to promote a culture of compliance. As set out in this Policy, all employees are responsible for the prevention and mitigation of bribery and corruption within their own roles and responsibilities.

In addition, every single employee of the Bank has been issued with a Code of Ethics containing guidelines that encompass a wide range of aspects, which, inter-alia, include the prevention of insider dealing in securities, outlines the internal rules on the purchase/sale of the Bank’s shares, notes down the Gift Policy, highlights how to manage conflicts of interest, provides information on combating financial crimes, and discusses the importance of respecting communities and the environment etc.

A detailed discussion is given in the section on Sustainable Banking – Value Creation.

Group Conduct Risk Management Policy Framework

During the year under review, the Bank adopted a Group Conduct Risk Management Policy Framework with a view to further strengthen risk management and corporate governance by ensuring that the Bank does not engage in any action that harms customers, negatively impacts market stability, and prevents effective competition. It is expected to establish a risk culture that not only addresses the risk of misconduct but also highlights clear accountability of actions through a preventive approach, by ensuring proper customer onboarding practices and transparency in fees and charges, and avoiding fraudulent activities, insider trading, improper financial advice to customers, mis-selling of financial products, tax avoidance, collusion with financial markets, and inaccurate financial and regulatory disclosures.

1. Principles referred to in this section are the principles in the Code of Best Practice on Corporate Governance – 2017 issued by CA Sri Lanka.