Introduction

Introducing our 54th Annual Report

The journey so far

Commercial Bank’s inaugural annual report, binding to the International <IR> Framework for integrated reporting, took shape in the year 2013. This Report comprising the Integrated Report and the Financial Statements is the 54th overall report and covers the period from January 01, 2022, to December 31, 2022, adhering to the annual reporting cycle for sustainability and financial reporting. This follows our most recent Report for the year ended December 31, 2021, for which comparatives are given, where applicable.

Heeding to the calls of various stakeholders, regulators as well as best practices, we have taken measures to be as concise as possible and to be as clear as we can, to meet the diverse information needs of our valued stakeholders. We have endeavoured to begin each section of this Annual Report with a clear and concise overview, that will extend to a narrative of the most important information pertaining to the Bank in 2022. Thereby, this Annual Report seeks to provide a holistic and integrated narrative of the Bank’s performance, operations, sustainability framework, and strategic imperatives, leading to sustainable value creation.

Navigating with prudence

We have delved into remedial interventions that the Bank employed to resist the pandemic and economic stresses that were felt throughout 2022. Stakeholders felt hardships at varying degrees, and the resultant landscape required bridging of varied expectations to the personalised delivery of banking utilities, to meet stakeholder hopes and aspirations. A detailed account of the measures implemented during the financial year is given in the Management Discussion and Analysis.

Transcending the medium to a handful of avatars

Consistent with last year’s report and the trends pertaining to modern annual report disclosures, and binding to the Swiss Army Knife model, our Annual Report has been made available in multiple mediums and formats catering to the communications needs of the Bank’s diverse stakeholder groups. A limited number of printed annual reports have been produced to be dispatched to those who have requested them, taking into to account the environmental footprint of printing a large number of reports as well as the prevailing regulations. Readers who prefer the ease of accessing our Annual Report online can access the Online Interactive version of the Annual Report while a soft copy (PDF) version is hosted on the websites of the Bank as well as the CSE for those who would like to maintain an easy-portable digital version. The Report can also be accessed by scanning the QR code given on page 2. This approach also aims to balance the disparate imperatives of conciseness, comprehensiveness, and accessibility in our disclosure practices.

The Online Interactive version of the Annual Report contains features to facilitate easy navigation across various sections of the Annual Report including unique Business Model of Financial Institutions, Statement of Capital Position, Duality of Value Creation, animated graphs, Notes to the Financial Statements that appear on a mouse over and hyperlinked cross references. Further, this version also includes the following user-friendly features;

- Customised graph generator

- “My Report” to build a customised report, print sections, download sections

- Download Centre

Irrespective of the medium, information is central to effective investor engagement. This Annual Report provides investors with insights into the Bank’s growth potential and the strategies by which the growth will be achieved.

Strategic focus and plurality of capitals

Sections 2.17 & 2.18 of the International <IR> Framework of the IFRS Foundation gives discretion to organisations to structure an integrated report and select capitals that suit the organisation most. Accordingly, this Report is structured based on the Bank’s 3-Pillar Approach to sustainability, viz. Sustainable Banking, Responsible Organisation and Community Sustainability, giving the reader a clear understanding of the Bank’s Sustainability Framework given and how it will help the Bank achieve the underlying purpose of “Being a responsible financial services provider by enabling and empowering people, enterprises and communities towards environmentally-responsible, socially-inclusive and economically-enriching growth”. How the activities undertaken under these three pillars and in terms of the four strategic imperatives of Prudent Growth, Customer Centricity, Leading through Innovation and Operational Excellence lead to value creation over short, medium and long-term for the mutual benefit of the Bank and the various stakeholders, which is reflected in Financial, Manufactured, Intellectual, Human, Social & Relationship and Natural Capitals is given on Statement of Capital Position. While assimilating the many efforts – mostly in inhospitable times – made by the Bank’s cross-disciplinary leadership into cohesive and convergent outcomes, this structure highlights the plotted course of action that will propel the Bank forward and sustain the value creation process while contributing to seven UN Sustainable Development Goals (SDGs) most relevant to the Bank in the context of certain guiding principles & standards and governance structure.

Criteria underlying the preparation of this Annual Report

- Strategic focus and future orientation

- Integrated thinking

- Non-financial information

- Guiding principles and frameworks

- Qualitative criteria

- Independent assurances

An integrated thinking cap

Commencement of integrated reporting in line with the <IR> Framework elements in 2013 has strengthened and reinforced integrated thinking across the Bank, leading to the integration of various aspects, making the Bank more sustainable in creating value over the long term by minimising risks, reducing compartmentalisation and dysfunctional behaviour, generating cost efficiencies, and making capital allocation more efficient. This not only integrated economic goals with those of society and environment, but also integrated many other aspects such as the following, as you will find later in this Report:

- Once a brick-and-mortar operation, the Bank in modernity is a digital superstore with a myriad of easy-to-use integrated products placed on digital shelves

- Repurposing of strategy with plans to pivot the business model to meet the emerging and disruptive forces of change

- The organisation from a functional and team-based one to a cross-functional integrated one

- Integrating service standards across all the channels leading to consistency in customer experience

- The Bank’s key messages across all communication channels for greater clarity

- Integrated software systems propelling the Bank to new standards of efficiency and agility

- Integrated audits combining onsite, offsite, online and near real-time approaches

- Integration of data from different sources to generate a unified view

- Information available across channels and products

- The Bank with other service providers such as telcos, insurers, other banks, Non-Banking Financial Institutions (NBFIs) and fintechs

Non-financial information

Recent trends make it clear that in addition to traditional forms of financial reporting, stakeholders in general, and providers of financial capital in particular, want access to non-financial information when assessing future potential of corporates. The Bank is well aware that information needs of stakeholders are changing in keeping with the dynamic environment we operate in. Investors in particular are increasingly becoming more interested in the future potential of the Bank than its past performance and non-financial information is becoming more and more relevant for ascertaining future potential. Accordingly, going beyond the historical financial information that depicts the value created in the past, we have enhanced disclosures of non-financial and future-oriented information that depicts the ability of the Bank to create value in the short, medium and long-term, the essence of sustainability and integrated reporting.

Basis of preparation

This Report has been prepared in line with the International <IR> framework, and the Bank’s social and environmental impacts are presented in accordance with the GRI Standards. It also comments on the Bank’s contribution towards the most relevant seven UNDP SDGs on Bank's Susstainability Framework.

The concepts, principles, and guidelines used in the preparation of this Annual Report are drawn from the following sources:

![]()

The International Financial Reporting Standards Foundation (IFRS)

(https://www.ifrs.org/)

![]()

The Global Reporting Initiative Sustainability Reporting

Guidelines – GRI Standards

(www.globalreporting.org)

![]()

A Preparer’s Guide to Integrated Corporate Reporting, published by

CA Sri Lanka

Handbook on Integrated Corporate Reporting, published by CA Sri Lanka in collaboration with The Integrated Reporting Council of Sri Lanka

Sustainability Framework of the Bank –

page 52

Report boundary

The Financial Statements given on pages 237 to 386 depict the consolidated performance of the entire Group, which includes the Bank along with seven subsidiaries – Commercial Development Company PLC, CBC Tech Solutions Limited, CBC Finance Ltd., Commercial Insurance Brokers (Pvt) Ltd., Commex Sri Lanka S.R.L. Italy, (under voluntary liquidation) Commercial Bank of Maldives Private Limited and CBC Myanmar Microfinance Company Limited – and the associate – Equity Investments Lanka Ltd.

The Bank’s social and environmental impact, elaborated within the Management Discussion and Analysis presented on Responsible Organisation - Shared Value, focuses on both Sri Lankan and Bangladesh operations of Commercial Bank of Ceylon PLC, the Parent entity of the Group which accounts for more than 97% of Group’s revenue, assets and deposits, unless stated otherwise.

Internal and external assessments of the Bank’s operations in Sri Lanka and in other countries such as Bangladesh are encompassed within the material aspects boundaries. The Bank always takes into account reasonable aspirations and expectations of its stakeholders and engages with them in myriad ways and they have been taken into account in deciding on the information content of this Report as depicted on “Connecting with Stakeholders” and “Material Matters”. Information is presented in a sustainability context, covering topics that reflect the Bank’s significant economic, environmental and social impacts that substantively influence stakeholder decisions. For the convenience of the stakeholders, quantitative and qualitative data along with reliable external benchmarks wherever possible has been provided to ensure completeness and aid comparison and further analysis of information within this Report.

During the year under review, no significant changes in the organisation type, structure, ownership, supply chain or topic boundaries took place. Also, there were no changes in reporting or restatements to the previously reported financial, social or environmental information.

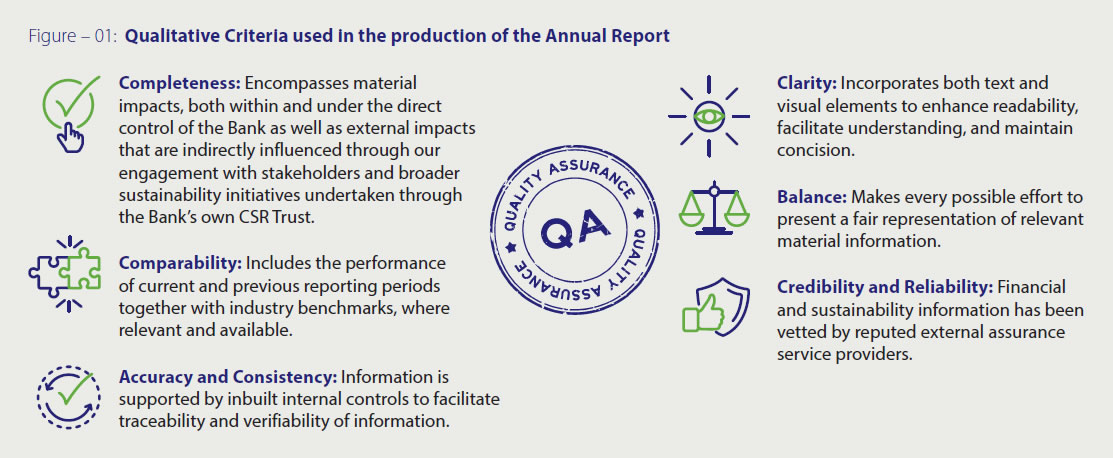

Quality assurance

Through this Integrated Report, we set out to provide you with a holistic and meaningful picture of our business model, Sustainability Framework, strategy, governance, performance, and future prospects. We also strive to illustrate the value created by the Bank in terms of non-financial resources such as Human, Natural, Intellectual, and Social and Network capitals, in addition to Financial capital.

In addition, every effort is taken to provide credible information with the aid of visual elements such as figures, graphs, and tables in a consistent manner facilitating clarity and comparability.

The qualitative criteria that were taken into account in the production of both text and visual elements presented in this Annual Report are given in Figure 01.

Precautionary principle

We are mindful of the direct and indirect social, climate and environmental ramifications of our operations, the indirect consequences resulting from the business activities of our borrowers in particular. We continue our de facto role to avoid, reduce and remedy any such negative impacts through the Bank’s Sustainability Framework viz., ongoing review of credit policies, stronger screening based on the Social and Environmental Management System (SEMS), close post-disbursement supervision, dedicated green portfolio of products and astute risk management procedures.

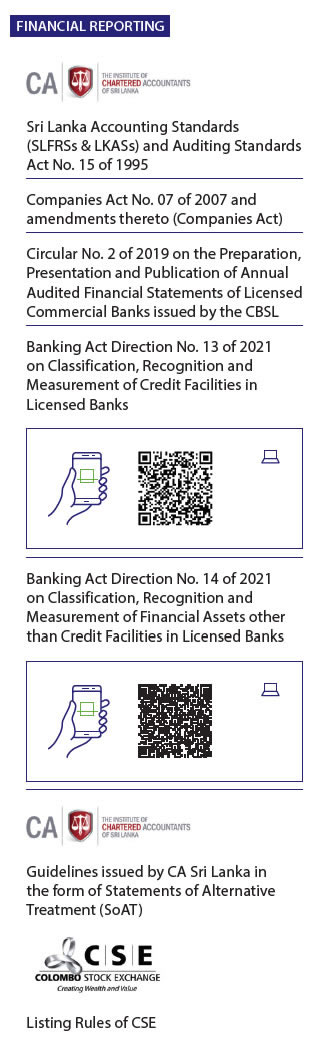

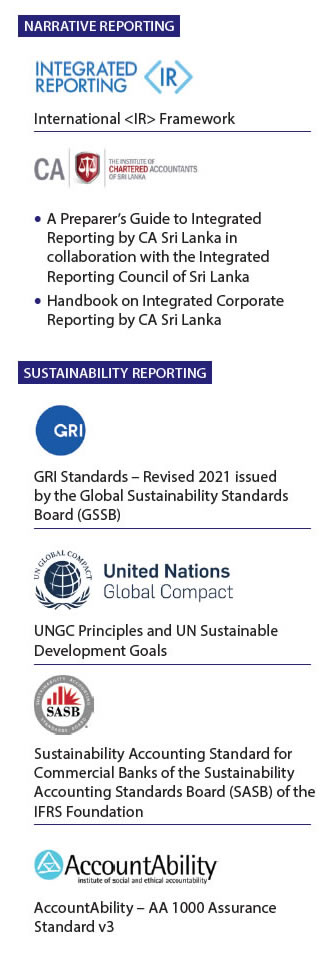

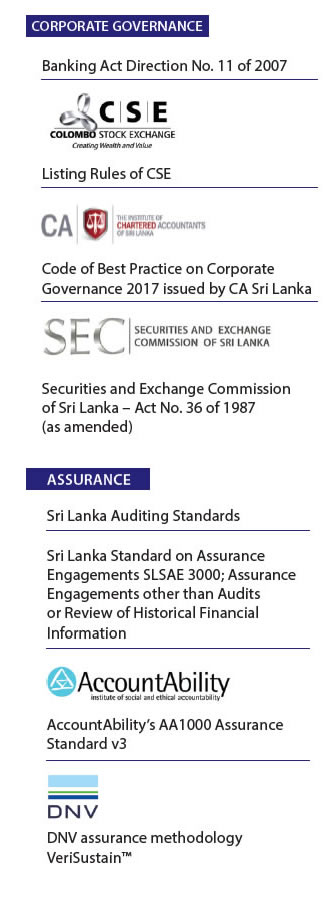

The Bank’s business model and operations do not directly create a significant negative impact on the environment. Nevertheless, every effort is made to reduce our own carbon footprint through initiatives such as solar energy usage, energy efficient air conditioning and the elimination of paper usage in our processes. These efforts enabled the Bank to become the first fully carbon neutral bank in the country in 2020 coupled with carbon credits while the Bank is on the way to become carbon neutral on its own. Figure 02 illustrates the guiding principles, regulations, codes, and Acts used for financial and narrative reporting; reporting on sustainability goals and practices; and the governance of the Bank.

Responsibility for sustainability practices and external assurance

Guided by the Bank’s Sustainability Framework, the Bank’s Managing Director/Chief Executive Officer, the Executive Director/Chief Operating Officer and other members of the Corporate Management are responsible for the sustainability practices and disclosures made in this Report. They have actively engaged with the external assurance providers on the Report content in this regard.

The Bank’s external Auditors, Messrs Ernst & Young, have assured the Group’s Financial Statements, integrated reporting and non-financial information on sustainability reporting, while Messrs DNV Business Assurance Lanka (Pvt) Ltd., who represents DNV, has assured the Bank’s non-financial reporting. The Board of Directors and the Management have no other relationship with these external assurance service providers, aside from their engagement as independent Assurance Service providers for the Group.

Figure – 02: Guiding Principles, Regulations, Codes, and Acts for financial and narrative reporting

Contact

Your comments or questions on this Integrated Report are welcome and we invite you to direct them to:

Chief Financial Officer

Commercial Bank of Ceylon PLC

“Commercial House”

No. 21, Sir Razik Fareed Mawatha

Colombo 01

Sri Lanka